The development of a background paper and the application of cost effectiveness indicators for use in Section 32 requests under Ontario Regulation 419: air pollution – local air quality

This report recommends a methodology for evaluating the cost effectiveness and relative effectiveness of potential air contaminant reduction techniques. It’s intended to support decisions regarding the appropriateness of potential air contaminant reduction techniques for industrial operations.

Cost Effectiveness Methodology

1.1 Introduction

This report recommends a methodology for evaluating the cost effectiveness of potential air contaminant reduction techniques as well as an indicator of relative effectiveness. The cost effectiveness methodology and indicator are intended to support decisions regarding the appropriateness of potential air contaminant reduction techniques for industrial operations.

Evaluation of air contaminant reduction techniques is based upon technical feasibility and effectiveness. However, the decision to implement is based upon efficiency and appropriateness. Efficiency is generally a measure of resources used (i.e. equipment, utilities, personnel, etc.). A contaminant reduction technique that is effective at reducing an air contaminant and uses resources effectively may be appropriate to implement.

Alternatively, a contaminant reduction technique that is effective at reducing an air contaminant, but uses resources inefficiently may be inappropriate to implement. The common measure of resources is cost. All resources can be converted into units of cost. Consequently, assessment of cost effectiveness of a potentially feasible technique would be valuable for informing a decision regarding appropriateness. Further, an indicator value that points to a threshold level at which cost effectiveness may be appropriate would provide an additional metric for a decision.

Importantly, cost effectiveness is a measure of efficiency in achieving an objective and not an evaluation of the benefit of achieving the objective. A cost effectiveness evaluation is not a cost benefit analysis. The recommended methodology presents a measure of the total resource effectiveness of a potentially feasible air contaminant reduction technique to be used as a tool in deciding the appropriateness to implement.

1.2 Background

Air management in Ontario changed significantly in November, 2005 with enactment of Ontario Regulation 419: Air Pollution – Local Air Quality (Regulation 419) and amendments in August, 2007. Regulation 419 establishes new or updated air standards based upon a scientific assessment of the health and environmental effects of contaminants. In the past, air quality standards were developed through a combination of scientific, technical and economic considerations. Under Regulation 419, technical and economic issues are now considered separately in the alteration of standards process set out in section 32.

A request for approval of an alteration to a standard for a contaminant in Schedule 3 of Regulation 419 may be made if circumstances listed in section 32 are applicable. A Schedule 3 air standard may be replaced with a site-specific standard that accounts for technical considerations and, if requested, economic feasibility. A request for approval of an alteration to an air standard must include the supporting information specified in section 32 of the regulation. Among other things, the request should include a technical benchmarking report for the identification and selection of methods that are best suited to minimizing Point of Impingement (POI) concentrations of the relevant contaminant. The request must demonstrate to the director of the Ministry of the Environment (designated under section 32, Regulation 419), that “best efforts” are being used to comply with the standard(s) set out in Schedule 3 of Regulation 419 and/or that POI concentrations are being reduced as much as possible. The Ministry’s Standards Development Branch (SDB) is responsible for development and implementation of the process to assess the acceptability of a request for approval of an alteration to a standard and may approve such requests pursuant to section 32(21) of Regulation 419.

1.2.1 Technology Benchmarking Reports

A technology benchmarking report is required to be submitted as part of a request for an alteration to a standard. Development of a technology benchmarking report and the identification of best practices is a regulatory requirement as set out in paragraphs 3 through 6 of subsection 32(13) of Regulation 419. Technology benchmarking is a key component of the Ministry’s risk-based approach to addressing situations where eligible facilities are requesting approval of an alteration to a standard. The purpose of a technology benchmarking report is to ensure that the actions taken represents best practices in limiting the POI concentrations and impacts of a contaminant(s).

Identification of available techniques and technology including an assessment of feasibility given site-specific considerations is required in a technology benchmarking report. The report should demonstrate a relatively thorough evaluation of available options to reduce POI concentrations of contaminant(s) for which an alteration to a standard is being requested. For significant sources of contaminant(s) a thorough review of POI reduction techniques should include an evaluation of the following:

- Materials: The assessment should consider a comprehensive review of the various potential raw material(s) used and how they affect emissions of contaminants of concern. Specific attention should be provided in identifying availability and feasibility of material changes that could reduce POI concentrations.

- Processes: The assessment should consider a comprehensive review of both processes and operating practices which emit the contaminant(s) that is the subject of the application in order to determine opportunities for POI reductions through a change in the overall approach to production; and inherently less polluting processes/practices or pollution prevention techniques.

- Add-On Controls: The assessment should include a review of add-on emission controls for each major source and major contributor to determine potentially feasible reductions of POI concentrations of the contaminant(s) that is the subject of the request.

Chapter 2.4 of the Ministry’s Guideline for the Implementation for Air Standards in Ontario (GIASO) outlines some of the factors to consider in developing a technology benchmarking report. Appendix A to the “Guide to Requesting an Alternative Air Standard” outlines a process for determining the best pollution control option, strategy, and/or combinations that will reduce the POI concentrations as much as possible.

A thorough and well constructed technology benchmarking report might identify multiple techniques, strategies and combinations of actions that could potentially reduce POI concentrations of contaminant(s) for which the alteration of standard is being requested. Of equal importance, the report should catalog technology(s) that have been considered and determined to be not feasible for the site’s specific circumstances. Ranking of potential options identifies the most effective techniques or combinations at reducing POI concentrations. However, evaluation and selection of potentially feasible site specific techniques and technologies may consider economic implications.

1.3 Economic Viability

There are broadly two categories of economic considerations in assessing potential technology changes to reduce POI concentrations. The first relates to a facility’s ability to afford potential changes to reduce POI concentrations. A facility may claim financial hardship and that economic viability of the enterprise would be jeopardized by implementing POI reduction actions. If a facility chooses to make an economic viability or hardship argument, in addition to the assessment of technical methods, as to why they are not able to comply with an air standard in Regulation 419, then an economic feasibility report is required to provide a clear rationale of the reason(s) why the facility cannot allocate sufficient funds to these compliance activities within the time frame or phase in period of the air standard set out by Regulation 419. The Director under section 32 of Regulation 419 may consider these arguments before a decision is made. The Ministry’s Guideline A-12: Guideline for the Implementation for Air Standards in Ontario (GIASO) outlines some economic indicators that can be considered in assessing overall economic feasibility (see GIASO chapter 2.5 and subsection 32(14) of Regulation 419).

As part of the Ministry’s Procedure F-14 (Economic Analysis of Central Documents on Private Sector and Municipal Projects, a facility must provide sufficient financial data to document and substantiate such claims. In situations where economic feasibility is an issue brought forward by a facility, the Ministry will consider the ratios in Table 4 of GIASO, as indicators of Financial Hardship for a facility and/or a company as well as other information to assess their situation on a case-by-case basis.

The former category of economic consideration is intended to provide a measure of how efficiently resources are used in achieving POI reductions leading ultimately to compliance with air standards set out in Schedule 3 of Regulation 419. This is a distinctly separate economic consideration from the latter category that evaluates site specific affordability of taking action.

1.3.1 Economic Considerations

The second economic consideration relates to using an economic evaluation to inform decision making in selecting the most efficient and cost effective action among competing options. The first relates to using an economic evaluation to inform decision making in selecting the most efficient of cost effective action among competing options. It is generally agreed that actions resulting in the greatest POI reductions that also cost less than other options are preferable. Similarly, the least cost option is preferable when selecting between equally effective options for reducing POI concentration(s). Extending the concept of using economic effectiveness in evaluating potentially feasible POI reduction techniques provides a valuable tool in selecting appropriate actions to implement. Presentation of a cost effectiveness methodology is the purpose of this report.

1.3.2 Transparency

Establishing a common framework for how site specific economic factors are to be organized and presented provides an excellent opportunity for an open and transparent assessment of potential POI reduction measures. The methodology should present sufficient details regarding cost and emission estimates to clearly demonstrate how cost effectiveness values were determined. An explanation of how potential POI reduction costs compare relative to indicator threshold values and the decisions obtained would open the process to all stakeholders.

1.3.3 A Uniquely Ontario Approach to Cost Effectiveness Required

Many jurisdictions use cost effectiveness to inform decisions regarding air pollution control measures. In the U.S., cost effectiveness is used extensively in regulatory development and assessing rule effectiveness. Considerable guidance is provided in the U.S. regarding how to perform cost effectiveness evaluations. However, the basis for these evaluations is typically to assess regional and national air quality performance whereas Regulation 419 deals with local air quality. European Union Best Available Techniques Reference Documents (i.e. EU BREF notes) provide similar direction to consider cost effectiveness, however, without the guidance provided in the U.S.. In addition, evidence exist that cost effectiveness considerations are used in Australia in selecting regulatory emission control measures without formal reference in available rules. All appear to use cost per ton of contaminant removed as the key measure of performance.

Regulation 419 establishes criteria focused upon local air quality and establishes air standards based on POI concentrations. Using a cost effectiveness methodology similar to the other jurisdictions resulting in cost per ton of contaminant removed would not provide information meaningful to concentration based air standards. A methodology unique to Ontario is required to evaluate cost effectiveness of potential POI reduction techniques.

1.4 Consideration of Risk Reduction

Consistent with the MOE's intent to use a risk-based process for alteration of standards, it is appropriate to consider the increased risk presented by operation of facilities over effects-based air quality standards in assessing cost effectiveness. In effect, more resources should be expended for greater potential risks posed by sources exceeding the effects-based air quality standards.

Earlier iterations of the proposed cost-effectiveness methodology included the addition of a toxicity scale to the denominator that would allow relative toxicity to be considered. The relative toxicity was proposed to be based upon USEPA's TRI relative toxicity scoring of chemicals Toxicity Score for cost effectiveness evaluation.xls. However, this approach was not pursued because numerous calculations involving three subject industry sectors, illustrated that the EPA’s toxicity scoring was not appropriate for use in the present methodology. For instance, there was not enough distinction between the toxicity of various metals.

Another method to assess risks may be a scale that considers the magnitude of the POI concentration, the frequency the effects-based standard being exceeded and the relative consequences of exposure. As contaminant specific risk factors increase, the amount of resources appropriate to reduce POI concentrations should also increase.

1.4.1 The Cost of Risk Reduction

There are other jurisdictions that use cost effectiveness to evaluate emission reductions. In Section 2 of this report, a summary of regulatory requirements in other jurisdictions is presented. The jurisdictional review included Canada, several U.S. states and USEPA, several European states and EU, and Australia. Cost effectiveness is used for a variety of purposes ranging from policy evaluation, to rule development, to individual source technology evaluation.

In the U.S., cost effectiveness is used to help identify and target sectors for further emission reduction efforts. Sectors identified as having sources of priority pollutants with cost effective control potential (low $/ton reduced) can be subject to additional regulatory effort to achieve regional and national air quality objectives. As a policy tool, cost effectiveness allows regulators to balance-out emission control costs between facilities and sectors by developing regulations that require equivalent expenditures in terms of cost per ton of pollutant controlled.

Regional and local administrators often use cost effectiveness to select required actions among competing options. Regulations in San Joaquin, California specify cost per ton required for specific pollutants (San Joaquin Valley Unified Air Pollution Control District BACT Policy, November 9, 1999,). While administrators in Australia have used cost effectiveness to select particulate control measures for diesel engines to achieve air quality improvements.

Technology reviews in the U.S. to demonstrate Best Available Control Technology (BACT) and Maximum Achievable Control Technology (MACT) rely heavily upon cost effectiveness to determine when to require additional emission controls. Cost effectiveness demonstrations are a routine part of many source approval evaluations.

In all cases, the use of cost effectiveness is a ratio of cost to implement and operate a control technology divided by the amount of emission reduction expected or $ per ton of emission reduction. Costs and emissions are evaluated on an annual basis and include operating and maintenance costs. This approach is not directly applicable to source evaluations in Ontario since the regulations focus on POI reductions and a desire to evaluate risk reduction potential. Specifically, further refinement of the denominator is required to translate emission reduction to the potential risk reduction. Fortunately, the Ministry’s Guideline A-12: Guideline for the Implementation for Air Standards in Ontario (GIASO) provides a starting point for risk estimation in the surrogate risk scoring methodology (see GIASO chapter 2.3 and Appendix II: A Risk Scoring Method).

1.4.2 Risk Scoring

The risk scoring method contained in GIASO provides a means of scaling the increased potential risk posed by facilities exceeding the effects-based standards. A dimensionless risk score is derived from the magnitude of the POI concentration, the frequency the effects-based standard is exceeded and a consequence weighting factor. The following formula is from GIASO;

R = RQ × Wcs × WL

Where,

- R

- a dimensionless risk score

- RQ

- Risk Quotient = [(Cmax)/MOE Standard]

- Cmax

- the maximum POI concentration (or at sensitive receptor with MOE approval)

- Wcs

- a weight assigned to one of the 6 consequence categories identified in Table A-1 based on the limiting effect of the MOE standard (or limit)

- WL

- percentage of time the model predicts an exceedence of the MOE standard (or limit)

The Wcs factor creates a weakness in using this risk scoring equation in deriving a cost effectiveness methodology. The consequence factor (Wcs) is a relative scaling of comparative ‘effects’ of different contaminants related to health and the environment. The intent of the risk scoring formula is to assist in prioritizing facility actions between competing sources and contaminants. The relative scaling of consequence factors is arbitrary, but directionally proportionate and useful in ranking options for priority action. Unfortunately, cost effectiveness must be assessed on an absolute scale to be of any value. Therefore, the consequence factor Wcs must be converted to an absolute scale if the risk score can be used to derive a cost effectiveness methodology.

Referring to GIASO Appendix II Table A-1: Consequence Categories Corresponding Weights (Wcs), the relative scaled ‘scores’ are proposed to be converted to absolute values by dividing each by the Medium Health score (7). Medium Health consequence represents the most significant (in terms of numbers) class of contaminants for which effects-based air quality standards have been developed. Further, it represents the category of contaminant that has been used to establish a cost effectiveness threshold value in the U.S. (this aspect will be expanded upon under competitiveness considerations). Assistance is provided in determining a contaminants primary ‘effect’ for purposes of standard development (i.e. Major Health, Medium Health, Minor Health, Major Environmental, Medium Environmental or Minor Environmental) in Appendix A to the Ministry’s “Guide to Requesting an Alternative Air Standard” (GRAAS).

To further simplify the absolute consequence scaling factors, the 6 categories contained in GIASO Appendix II have been reduced to 3 categories; namely, Major Health (10/7 = 1.43), Medium Health (7/7 = 1.00) and Environmental and Minor Health (6/7 = 0.86).

The risk score with adjusted consequence scores may be used to evaluate cost effectiveness of potential POI reduction techniques.

1.5 Competitiveness Considerations

Local air quality considerations may direct decisions on a facility specific basis. However, competitiveness between facilities needs to be considered. Development of a cost effectiveness methodology should not result in a cost burden that places Ontario facilities at an economic disadvantage with competing facilities in adjoining jurisdictions. Ontario facilities compete on a global basis, but first and foremost on a regional basis. Ontario facilities share labor and transportation costs common with U.S. Mid-Western states and emission control cost effectiveness requirements should be similar to avoid competitive disadvantage.

In the U.S., a cost effectiveness threshold value of $10,000 per ton of Medium Health effect contaminant has been declared by the President (Presidential Documents, Federal Register, Vol.62, No.138, Friday July 18, 1997, and reiterated by the USEPA Administrator (Mary Nichols, Assistant Administrator for Air and Radiation, EPA, Ozone and PM Standards, July 24, 1997). This is a policy declaration that continues in effect to this day. This is the declared level of expenditure that is used for evaluating regulatory requirements to achieve further reductions of priority pollutants. That is, regulations may be developed to require further emission reductions as long as they do not cost more than $10,000 per ton to achieve. This would appear to represent a good calibration point for evaluation of effective resource utilization in Ontario.

1.6 The Cost of Technology

The cost of implementing and operating a potential POI reduction technique must be completely and thoroughly inventoried. All costs associated with bringing the technique ‘on-line’ should be included.

Capital costs associated with the purchase and installation of equipment should be estimated. Vendor bids, quotes, engineering estimates and extrapolations from similar installations can provide excellent sources of cost information. The key is to be thorough in identifying all equipment associated with the reduction technique. Initial directional cost estimates may provide enough detail to complete an assessment, more precise information can be added later if needed.

Operating and maintenance should be included in assessing potential POI reduction techniques. These are the on-going costs associated with operating the equipment and/or processes. They may include additional operating and maintenance labour, additional utilities (i.e. water, electricity, natural gas, compressed air, etc.), and materials (i.e. more costly ingredients with less contaminants of concern, added chemicals to improve process performance, replacement parts, etc.).

Cost savings or revenues should also be considered in assessment of annualized costs. Some POI reduction techniques may result in operational efficiencies that save costs. These should be identified, quantified and included as a reduction in cost

1.6.1 USEPA OAQPS Control Cost Manual

USEPA Office of Air Quality Planning and Standards (OAQPS) has developed an excellent manual that provides a thorough listing of elements to consider in evaluating the cost of implementing a emission control technique. The manual is a widely used reference and is updated periodically to keep it relevant and current. Importantly, the manual contains extensive survey information providing routine and customary pricing of many of the elements required for installation of a variety of air pollution control devices. The cost estimating formulas and factors provide good directional estimates, but care should be exercised in understanding their limitations. Source specific engineering estimates can often provided better cost estimates but must be provided for review.

OAQPS’ EPA Air Pollution Control Cost Manual (Sixth Edition), EPA/452/B-02-001 is available online.

1.7 Total Resource Effectiveness

Bringing together the various concepts from other jurisdictions and the risk-based assessments involved in evaluating alteration of standard(s) requests results in a unique Total Resource Effectiveness (TRE) approach to cost effectiveness. A dimensionless ratio is created by dividing the Total Annualized Cost (TAC) (or the Net Total Annualized Cost (NTAC) if there are savings involved) estimated to implement a potential POI reduction technique by a threshold of Risk Reduction Cost (RRC). Using site specific information obtained from the facility’s Emission Summary and Dispersion Modelling report (ESDM), a risk score is calculated (based upon an assessment of the consequence, frequency and magnitude of exposure). This is then combined with the POI reduction potential and a cost factor to determine a facility specific RRC value. The following equation results:

TRE = TAC / RRC

Where,

- TRE

- Total Resource Effectiveness a dimensionless value

- TAC

- Total Annualized Cost of potential POI reduction technique

- RRC

- Risk Reduction Cost = R × EER × 104

Where,

- R

- RQ × Wcs × WL

- R

- a dimensionless risk score

- RQ

- Risk Quotient = [(Cmax)/MOE Standard]

- Cmax

- the maximum POI concentration (or at sensitive receptor with MOE approval)

- Wcs

- either 1.43 (Major Health), 1.00 (Medium Health), or 0.86 (Environmental or Minor Health)

- WL

- percentage of time the model predicts an exceedence of the MOE standard (or limit)

- EER

- Equivalent Emission Reduction is the potential POI improvement achievable by the technique being evaluated

- 104

- $10,000

The TRE value provides an indicator of relative acceptability of a potential POI reduction option given site specific considerations. Notably, if the TRE value for a specific POI reduction option is equal to or less than 1.0, then it represents an acceptable use of resources and should generally be implemented. TRE values falling between 1.0 and 10.0 would generally warrant closer evaluation of all the underlying assumptions and further consideration of site specific factors. However, TRE values greater than 10.0 would generally represent poor use of resources and should not be implemented.

Three important factors are incorporated in the TRE value for evaluating potential POI reduction options. First, it considers economics both as it relates to the cost of implementing reduction measures and cost that is acceptable for reducing risk based upon the site specific characteristics of the contaminant. Secondly, the TRE value incorporates the magnitude of the potential POI reduction in a normalized equation that allows for comparison of a full range of options regardless of size. Last, the TRE value provides a threshold of general acceptability that informs decisions regarding the appropriateness of potentially feasible POI reduction options.

1.7.1 TRE Calculation Forms

Innovative yet simple spreadsheet type forms have been created to allow easy estimation of TRE values based upon information that should be readily available to facilities preparing to request an alteration of standard. The simple “one-page” form has been created for common add-on control devices (i.e. regenerative thermal oxidizer, pulse-jet filter house and venture scrubber). Blank forms are attached (Attachment 2). The forms may be used to calculate a TRE value with the following source information;

- System air flow capacity,

- Source operating hours,

- Estimate of initial equipment cost,

- Risk Score based upon data from the facility’s ESDM,

- Estimate of annual emissions before reduction,

- An estimate of POI reduction potential.

The resulting value may be used as a screening tool to provide an initial indication of TRE for potential control option(s). Further refinement of the TRE value can be obtained by substitution of site specific engineering and cost information. The form can be easily modified to estimate the effectiveness of other types of POI reduction techniques (i.e. material and/or process changes). The principle attribute of the form is that it allows an estimate of a TRE value for a source with minimal effort.

1.7.2 Line by Line TRE Calculation Form Explanations

The following narrative describes the elements necessary to calculate a TRE value. Each element corresponds to a data element contained in the simplified TRE calculation form and the reader may find it useful to refer to the form while reviewing the following descriptions.

1.7.3 Total Annualized Cost (TAC)

Without experience or guidance, estimating potential costs associated with purchasing, installing and operating air emission control devices can be a daunting task. Fortunately, excellent reference material is available from the USEPA Office of Air Quality Planning and Standards (OAQPS) that provides direction on cost elements to consider and extensive survey information providing routine and customary pricing of many of the required elements. OAQPS' EPA Air Pollution Control Cost Manual (Sixth Edition), EPA/452/B-02-001 is available online. The manual is periodically updated so it is recommended that the latest version be used.

Estimating the cost of controls should include both direct and indirect costs associated with purchasing and installing equipment. These costs are typically one time expenditures described as capital costs. The one-time costs should be normalized to equivalent annual expenditures to facilitate evaluation of total expected annual costs. Simple equal uniform annual cash flow of capital investment at a 6 percent recovery rate over a 10-year period is used for this purpose, as specified in the Ministry’s GIASO document . Similarly, both direct and indirect annual operating and maintenance costs are estimated. These are recurring and on-going costs associated with operating the technology. The summation of annualized capital costs and annual operating and maintenance costs represents the Total Annualized Cost (TAC).

1.7.4 Capital Costs

1.7.4.1 Purchased Equipment Cost

- Control Device

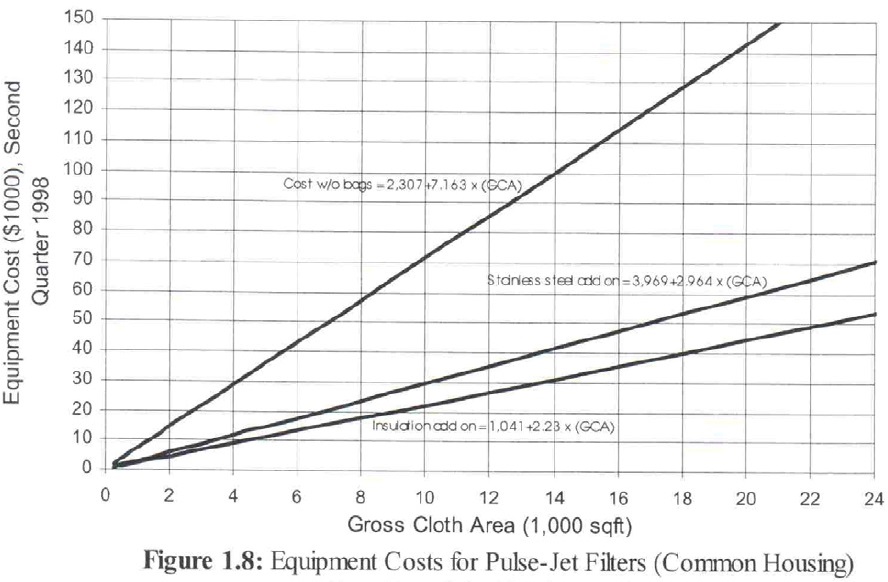

Purchase cost is estimated for the primary pollution control device. Typically this represents the base device such as a filter house or oxidizer without supporting equipment. Extensive surveys of equipment manufacturers and purchasers of equipment have resulted in graphs indicating approximate cost of equipment based upon the quantity of air being handled. Graph 1 represents typical data available for Pulse Jet type filter houses. Typical data for Thermal Oxidizers is presented in Graph 2. Graph 1 and 2 are from the OAQPS manual.

Graph 1 Typical Available data for Pulse-Jet Type Filter Houses

(Equipment Costs for Pulse-Jet Filters [Common Housing])

Note: GCA = Gross Cloth Area in square feet.

Source: ETS Inc.Graph 2 Typical Data Available for Thermal Oxidizers

- Auxiliary Equipment

This item represents an estimate of the cost of equipment needed to allow the control device to function. This could include components such as hoods/enclosures, ductwork, motors, fans, valves, exhaust stacks, safety by-pass equipment, etc. The OAQPS Control Cost Manual contains formulas and techniques for estimating costs for many of these items. Vendor quotes for supplying control devices often include these items in the direct purchase price and estimates may not be required separately. Auxiliary equipment can typically range from 80 to 120 percent of control device costs with even higher percentages expected as the primary device gets smaller.

- Instrumentation

Often the control device is complex mechanical equipment requiring electronic and/or computerized instrumentation to control. Occasionally, continuous emission monitors or process monitors (temperature, leak detection, etc.) are required and cost estimates are included here. Sometimes instrumentation costs are included with the control device, especially if the cost estimate is from a vendor quote for ‘off-the-shelf’ equipment. Typical cost could be about 10 percent of cost of the control device and auxiliary equipment combined.

- Taxes

Sales taxes apply for most equipment purchases. In Ontario, PST and GST have been estimated at 13 percent of the cost of the control device and auxiliary equipment combined.

- Freight

The cost of shipping equipment needs to be included in the purchased cost estimate. Depending on the size and distance that equipment must be shipped, this can be a significant cost item. Typical costs have been estimated at 5 percent of the cost of the control device and auxiliary equipment combined.

The base price (C) of purchased control equipment is then the sum of items a. through e.

1.7.5.1 Direct Installation Costs

- Foundation and Support

Control devices, ducts, stacks, etc. are often large and heavy requiring addition of structural foundations and supports. Frequently equipment is placed on building roofs requiring installation of reinforced columns and structural steel trusses, etc. Typical costs are estimated at 4 and 8 percent of the base price for filter houses and thermal oxidizers, respectively. Oxidizers being relatively smaller and heavier require slightly more structural support.

- Handling and Erection

Equipment must be delivered, staged and installed. Cranes must be used to move large/heavy components, and welding, bolting and fitting must be completed. Typical costs are estimated at 50 and 14 percent of the base price for filter houses and thermal oxidizers, respectively. Filter houses typically involve far more field construction and fabrication than oxidizers that are largely shop fabricated and shipped ready to install.

- Electrical

Electrical service must be provided and connected to power motors and instruments. This item includes wiring, buses, switches and transformers required to service the control device as well as the electricians to perform the work. Typical costs are estimated at 8 and 4 percent of the base price for filter houses and thermal oxidizers, respectively.

- Piping

Gas lines, stream lines, compressed air, water lines (for the control device and/or fire suppression) and drain lines may be required. Typical costs are estimated at 1 and 2 percent of the base price for filter houses and thermal oxidizers, respectively.

- Insulation

Ductwork and/or piping may require insulation for thermal efficiency or condensation control. Typical costs are estimated at 7 and 1 percent of the base price for filter houses and thermal oxidizers, respectively.

- Painting

Corrosion protection painting of structural elements, some ducts, piping, tanks, control device, etc. may be required. Typical costs are estimated at 4 and 1 percent of the base price for filter houses and thermal oxidizers, respectively.

- Site Preparation

Primarily the related cost associated with clearing obstructions and making space available to receive the new equipment. This is completely site specific and no attempt has been made to estimate routine or customary values. Site specific justification is required to estimate costs here.

- Facilities & Buildings

Occasionally significant ‘infrastructure’ type work is needed to accommodate a new control system. Items such as control device waste handling equipment, boilers to make steam, compressors for air, building additions to house sensitive equipment, etc. Similar to Site Preparation, this is a completely site specific item and no attempt has been made to estimate routine and customary values. Site specific justification is required to estimate costs here.

- Retrofit Costs

Installation of new control equipment into an existing facility can lead to major design and installation changes. Issues such as not enough room to install equipment or special provisions to accommodate available room are related to retrofit. Retrofit costs are not contingencies, which are unexpected costs related to purchasing and installing equipment (addressed elsewhere). Usually carried as a percentage of the total capital cost, USEPA has retrofit costs as high as 30 to 50% for some situations in the OAQPS manual. Higher costs have been used in some MACT standard development documents. Care must be taken in estimating retrofit costs so as to not double count costs. If extra costs are estimated for activities such as foundations, structural supports, erection, electrical, site preparation, facilities & buildings, etc. because of existing conditions then retrofit costs should be correspondingly lower. Site specific justification is required to estimate costs here.

The Total Direct Cost (DC) is then the summation of elements a. through n.

1.7.5.2 Indirect Installation Costs

- Engineering

Design and field support for installation. Typical costs are estimated at 1 percent of the base price for both filter houses and thermal oxidizers.

- Construction and Field Expenses

Costs associated with personnel and miscellaneous costs to fully install and commission the control system. Typical costs are estimated at 20 and 5 percent of the base price for filter houses and thermal oxidizers, respectively. Installation of filter houses is generally a more complicated process because of the greater level of field fabrication involved.

- Contractor Fees

This is contractor profit and is typically estimated to be about 10 percent of the base price of the equipment.

- Start-up

Cost associated with initial placing of the system into operation, adjustments and turn-over of a functioning control system to the facility. Typical costs are estimated at 1 and 2 percent of the base price for filter houses and thermal oxidizers, respectively.

- Performance Test

Testing cost to assure the control device and the system functions as purchased. Compliance testing to demonstrate performance to regulatory agencies may be included in this item. Typical costs are estimated at 1 percent of the base price.

- Contingencies

Provision is provided for unanticipated cost increases. Typical costs are estimated at 3 percent of the base price.

Total indirect costs (IC) are obtained by summing items o. through t.

Total Capital Investment (TCI) = C + DC + IC.

Capital Recovery Cost (CRC) = 0.13587 × TCI. The capital recovery factor is obtained from 6% recovery over a 10-year period and projected as equal uniform annual cash flow of the capital investment, as prescribed in the Ministry’s Guideline for the implementation of Air Standards in Ontario (GIASO).

1.7.6 Annual Operating and Maintenance (O&M) Costs

1.7.6.1 Direct Annual Costs

- Operating Labor (OL)

Estimated hours per year required to operate the POI reduction system or control device multiplied by the hourly operating labor cost. For the simplified example calculation, $30 per hour is used to estimate the hourly labor rate including direct pay and benefits.

- Supervisory Labor (SL)

Annual cost estimate for direct supervision of control system operators should be provided. A reasonable estimate for supervision is obtained by using 15 percent of the operating labor cost and has been applied in the simplified example calculation.

- Maintenance Labor (ML)

Estimated hours per year required to maintain the POI reduction system or control device multiplied by the hourly maintenance labor cost. For the simplified example calculation, $40 per hour is used to estimate the hourly rate for direct pay and benefits which is slightly higher than the operating labor rate to reflect the use of skilled trades.

- Maintenance Materials (MM)

Maintenance of equipment requires the consumption of a wide variety of routine replacement and consumable items such as oil & grease, nuts and bolts, hand tools, washers and gaskets, etc. An estimate of the annual cost for these items is provided here. Typical cost is estimated to be equivalent to maintenance labor cost.

The Direct Labor Cost (D) is then obtained by the summation of elements a. through d.

- Replacement Parts

The purchase of parts and components to replace worn out or broken equipment throughout the life expectancy of the equipment is estimated here. These are items beyond the consumable maintenance materials and include items such as replacement filters for a bag house, heat exchange media for a regenerative thermal oxidizer, spare motors and valves, bearings, VFDs, etc. In addition to larger components that are maintained in facility inventory to shorten repair time, long lead time spare parts may be in this estimate.

- Utilities

An estimate should be provided to quantify the increased consumption of utilities to support operation of the POI reduction technology. These are recurring costs that can represent a significant element in evaluating the appropriateness of a potentially feasible control technique or technology. Generally, estimating utility costs will require a measure of engineering judgment without more detailed design information that is typically not available at the technology evaluation stage. Some examples include;

- Natural Gas – Anticipated annual consumption multiplied by a unit cost. Fuel burning equipment such as thermal oxidizers used to destroy volatile organic contaminants can consume large quantities of natural gas. Based upon the size of a thermal oxidizer determined by the quantity of air flow being controlled a directional estimate of the amount of natural gas required and cost to operate the device may be obtained. For the simplified example calculation it has been assumed that highly efficient thermal recovery devices will be used providing the capability of recovering all but 100°F of the heating value of the oxidizer operation. An estimate of the cost of natural gas has been made at $7.00 per MCF. Similar estimates can be made for other control techniques.

- Compressed Air – Compressed air is required primarily for filter houses, for cleaning filters. The amount of compressed air required is calculated by multiplying the total air flow by the pulse of compressed air required. The simplified example calculation estimated 2 cfm pulse/1000 cfm airflow. The typical cost estimate is $0.25/1000 cfm

- Electricity - Anticipated annual consumption multiplied by a unit cost. Fans are required to move air to and from most control devices and are powered by motors that can consume large amounts of electricity. Other components such as powered dampers and valves and electronic/computer controllers consume electricity, but are generally small relative to motors. Many factors affect the efficiency with which motors consume electricity and detailed engineering is required for proper sizing and design. However, directional estimates can be made. The simplified example calculation estimated 3 hp/1000 cfm of air. The KWH of electricity required were calculated through a simple conversion of hp. The cost estimate used was $0.08 per KWH. It should be noted that 3 hp/1000 cfm may seem high but the cost of running other electrical devices such as powered dampers and valves and electronic/computer controllers were not included.

Total Direct Cost is then the sum of items a. through f.

1.7.6.2 Indirect Annual Costs

- Overhead

Organizational overhead costs for operating labor and maintenance. These are the fixed facility operating costs that increase as the number of employees increase. Typical costs are estimated at about 60% of Direct Labor Costs.

- Administrative Charges

This is an attempt to estimate overhead costs not specifically tied to facility operation such as sales, research and development, accounting, and other home office expenses (not plant overhead). Typically these are estimated at 2% of the projects Total Capital Costs.

- Property Taxes

Fixed assets are normally subject to property taxes. In Ontario, this value has been estimated at 1% of Total Capital Costs which is typically used as an approximation for directional projections.

- Insurance

A simplified estimate for facility and equipment loss protection is obtained with a value of 1% of Total Capital Costs.

Total Annual O&M Costs (OMC) is a sum of indirect and direct annual O&M costs, or a sum of items a. through j.

Total Annual Cost Savings (SAV) is the sum of annual cost savings that may result from implementing a POI reduction technique. Efficiency projects can result in labor and utility reductions or material use savings. These costs should be identified and recorded and the overall cost of the proposal being evaluated reduced equivalently.

1.7.7 Total Annualized Costs

An estimate of the total annual cost (TAC) of purchasing, installing and operating equipment to obtain POI reduction may be obtained by summing the Capital Recover Cost, CRC (i.e. the capital cost spread-out evenly over a 10-year period at a 6% rate of investment return) and annual operating and maintenance cost (OMC) less any cost savings (SAV) identified.

TAC = CRC + OMC − SAV

Annualizing capital cost provides a convenient time frame for combining with operational and maintenance costs which are traditionally planned as yearly recurring expenses. Seasonal variations may also be normalized by using an annual period.

1.7.8 ESDM Information

The total annualized cost of a potential POI reduction technology is to be evaluated relative to a threshold risk reduction cost. Consistent with the Ministry’s risk-based approach to evaluating alteration of air standard requests, the consequence of exposure to a contaminant(s) of concern should be considered in determining the threshold Risk Reduction Cost (RRC).

- Source Emission Before Change

It is important to establish a baseline condition for evaluating potential improvement options. The facility’s ESDM will establish current source conditions resulting in the request for an altered air standard. This value is presented as an annual emission in units of tonnes. The purpose of this value is to establish potential contaminant reduction options on an annual basis consistent with annualized cost estimates.

- Maximum POI Concentration

The facilities dispersion model will predict a maximum POI concentration (POI Cmax) for each contaminant evaluated, this value should be entered on the form. Alternatively, it may be appropriate to use the maximum concentration at a sensitive location, with the approval of the Ministry.

- MOE Standard

The effects-based MOE standard for the contaminant for which the evaluation is being performed should be entered on the form.

- Frequency of Exceedence

The facilities dispersion model will predict the frequency with which the MOE standard would be exceeded based upon operating conditions and the meteorological data set utilized (Note: site specific approved meteorological data must be used to assess frequency of exceedences). The frequency value is expressed as a percentage and should be entered on the form.

- Consequence Score

A consequence score based upon the assignment of a contaminant to a category as defined in information presented in Appendix A to the Ministry’s “Guide to Requesting an Alternative Air Standard” (GRAAS) is entered on the form here. The value will be either 1.43 (Major Health), 1.00 (Medium Health) or 0.86 (Minor Health or Environmental). An explanation regarding derivation of these values may be found in the Risk Scoring section 1.4.2 of this report.

- Risk Quotient

The ratio of maximum POI concentration to the MOE standard is described as the risk quotient and is automatically calculated by the form.

- Risk Score

The risk score for the facility is calculated as the product of Risk Quotient (line f. value), Consequence score (line e. value) and frequency of exceedence (line d. value). The risk score value is automatically calculated by the form.

- Potential POI Improvement

Potential add-on emission control device performance is often expressed as removal efficiency. However, other techniques for reducing contaminant emissions may also be expressed as percent improvements (i.e. material substitutions and process changes), in the technology evaluation stage, estimating performance of a reduction technique may involve approximation of improvement by comparison to other similar sources. Estimation of reduction efficiency across a board range of options is most easily expressed as a percent reduction. Importantly, other source changes that could result in reduction of POI concentrations may be expressed by percent improvement. Source changes such as relocation of exhaust points within a facility can result in significant reduction to projected POI concentrations. While source relocation may not reduce contaminant emissions, its virtual effect may still be expressed as a percent reduction. The estimated percent improvement for the source attributed to the evaluated reduction technique is entered into the form here.

- Equivalent Emission Reduction (or % POI Reduction)

The potential emission reduction of the contaminant(s) reduction technology(s) or technique(s) is simply the product of available emissions (line a. Source Emission before Change) and the reduction potential (line h. Potential POI Improvement). Some POI reduction techniques are not the result of source reductions. Source relocations and exhaust point changes are examples of changes that may reduce POI concentrations without source reduction. However, the POI improvements may still be expressed as virtual reductions for the purposes of evaluating TRE. The value is automatically calculated by the form and entered at line i.

1.7.9 Threshold Risk Reduction Cost (RRC)

A threshold of annualized risk reduction cost is expressed as the product of site specific risk score, site specific contaminant reduction potential and a cost factor. The cost factor used is $10,000 per tonne, which is adjusted upward or downward based upon consequence of potential exposure as expressed by the risk score. The formula is expressed as:

RRC = Risk Score × Potential POI reduction (tonne) × $10,000/tonne

The value is calculated automatically by the form.

1.7.10 Total Resource Effectiveness (TRE) Value

As described previously, the Total Resource Effectiveness Value is determined by the ratio of Total Annualized Cost (TAC) for a potentially feasible POI reduction option to the threshold Risk Reduction Cost (RRC) derived to express the consequence of exposure to a contaminant considering site specific conditions.

The TRE value presents a measure of economic feasibility in close consideration of the consequence of exposure to contaminant(s), using the risk scoring methodologies established in the Ministry’s GIASO document. The TRE methodology provides a consistent approach that is both open and transparent to all stakeholders, for facilities to evaluate cost effectiveness of potentially feasible control options.

1.7.11 Example TRE Value Calculations

Application of the total resource effectiveness calculation methodology may be best illustrated through example. With relatively limited source information, creditable estimates may be derived to evaluate the effectiveness of resource utilization in achieving POI reductions. The source information is readily available from a facility’s ESDM report. Potential POI reduction techniques are identified through the facility’s Technology Benchmarking Review. Cost information may be obtained from a variety of sources. USEPA's Control Cost Manual provides a wealth of information needed to estimate the cost of a wide range of add-on emission control devices. Other sources (i.e. engineering texts, trade publications, research publications, etc.) may also provide useful information. Vendor quotes to provide equipment and/or service can provide the highest quality cost information, but may be the most difficult to obtain when performing feasibility evaluations. Most importantly, engineering judgment is required throughout the process of assembling information and costing potential POI reduction techniques. Forms that add structure and format to assembling and presenting cost effectiveness information can aid (but not replace) the environmental professional’s judgment.

Three (3) example calculations will be presented to help illustrate the application of the TRE methodology and use of the indicator value to aid evaluation of potential POI reduction techniques. The first two examples evaluate the appropriateness of installing add-on control devices to reduce emissions. The first source is evaluated for particulate emission reduction and the other source for volatile organic compound reduction. The third example will illustrate how the methodology may be utilized to evaluate a process change as a potential POI reduction technique.

Example 1

A facility operates a process that generates a significant quantity of particulate emissions. The facility has provided the process with a hood and ventilation system to capture fumes and direct them to an existing filter house to reduce particulate emissions. In this example we utilize available information to evaluate the reasonableness of the facilities decision to install and operate the emission control device using the TRE methodology. This example provides an opportunity to ‘ground truth’ the TRE methodology and indicator value versus existing decision making.

From the facility’s ESDM it is determined that the source exhausts 0.1 g/s of particulate material contained in 57,000 cfm of process air. The facility intends to operate the source without restriction (i.e. 8,760 hours per year). For this example, it will be assumed that the facility is exceeding the TSP standard of 100 µg/m3 and operating in the mid-ALARA region (i.e. 5 times the standard, 50% of the time).

Refer to Figure 1 in Attachment 1 to see how the calculations proceed when the information is entered. Data entered into the form is highlighted in blue for clarity. Those values not in blue are automatically generated by the form.

Turning to USEPA's Control Cost Manual, Section 6, Chapter 1 Particulate Controls for assistance with estimating control costs the following calculations are performed.

Control Device

Based upon the source to be controlled and engineering judgment it is decided to evaluate a pulse jet type filter house operated under positive pressure using fiberglass filters. In addition, it is assumed that the exhaust air temperature will be below 500°F, so no pre-filter cooling is required. Further, a gas to cloth ratio of 6 will be assumed to approximate the filter area required. Other filter types, materials and ratios could be chosen, but these have been selected for this evaluation. So, initial filter house sizing is determined by the following calculation;

57,000 cfm/6 (gas to cloth ratio) = 9,500 sq. ft. × 1.5 (Table 1.2) = 14,250 sq. ft.

{Table 1.2 values are used to convert net filter area to gross or required surface area.}

Next, using regression formulas derived from actual cost data collected by USEPA, an estimate of the pulse-jet filter house control device cost may be calculated.

From Figure 1.8, Pulse-Jet Filters (Common Housing);

Filter house cost − 2,307 + 7.163(14,250) = $ 104,380

Added cost for stainless steel construction − 3,696 + 2.964(14,250) = $45,933

{Stainless steel construction is selected for durability given the source being evaluated}

From Table 1.8: Bag Prices - Fiberglass filters using bottom bag removal, $1.69/ft2;

14,250 × 1.69 = $24,083

Further, from Table 1.8: Bag Prices – Assume stainless steel cages 5 1/8 inches × 10 feet;

5 1/8 inches / 12 × 3.14 × 10 = 13.4 sq. ft./cage

14,250/13.4 = 1,063 cages required

[8.8486 + 1.2284(13.4)] × 1,063 = $26,904

An estimate of the control device cost is then the sum of these four values;

104,380 + 45,933 + 24,083 + 26,904 = $201,300

Auxiliary Equipment

The control device cannot reduce TSP emissions without a fume capture hood, ventilation ducts, fans, motors and exhaust stack. Cost estimates can be made for these elements by using regression formulas contained in USEPA's Control Cost Manual, Section 2, Chapter 1. The following cost calculations are performed;

Fume Capture Hood

From Equation 1.40,

C = aAfb

Where,

- C

- Cost ($)

- a

- 306 - Table 1.8 Canopy rectangular

- b

- 0.506 - Table 1.8 Canopy rectangular

- Af

- Face area of hood (ft2) = air flow (cfm)/500 fpm

{500 fpm is selected to achieve suitable fume capture velocity}

This cost estimate is not used for this example since an existing hood is in place yielding the reported capture efficiency and emission rate. Making a change to the basic capture system design would introduce undesirable inaccuracy to the ESDM reported emission information for this example. The existing capture hood will be assumed to remain in service.

Ventilation Duct

From Equation 1.40,

C = aDb

Where,

- C

- Cost per foot of duct ($)

- a

- 1.56 - Table 1.9, stainless steel circular

- b

- 1.00 - Table 1.9, stainless steel circular

- D

- Duct diameter (inches) = air flow (cfm)/4,000 fpm

{4,000 fpm is selected to keep PM suspended in duct}

Then,

57,000/4,000 = 14.25 sq. ft.

Diameter = SQRT[(4 × 14.25)/3.14] = 4.3 feet or about 52 inches

1.56(52)1.0 × 100 feet = $8,112

{100 feet of duct assumed for this example}

Duct Elbows

From Equation 1.41,

C = aebD

Where,

- C

- Cost per elbow ($)

- a

- 74.2 - Table 1.10, stainless steel elbows

- b

- 0.0668 - Table 1.10, stainless steel elbows

- D

- Duct diameter (inches)

Then,

74.2e(0.0668 × 52) × 4 = $9,573

{4 elbows assumed for this example}

Ventilation Dampers

From Equation 1.41,

C = aDb

Where,

- C

- Cost per damper ($)

- a

- 208 - Table 1.10, Aluminized CS louvered with actuators

- b

- 0.791 - Table 1.10, Aluminized CS louvered with actuators

- D

- Duct diameter (inches)

Then,

74.2e(0.0668 × 52) × 4 = $9,573

{4 elbows assumed for this example}

Stack

From Equation 1.41,

C = aDbL

Where,

- C

- Cost ($)

- a

- 12.0 - Table 1.12, Plate stainless steel

- b

- 1.20 - Table 1.12, Plate stainless steel

- D

- Stack diameter (inches)

{3,000 fpm stack exhaust velocity assumed for proper dispersion,

57,000/3,000 = 19 sq.ft.

Then,

- D

- SQRT[(4 × 19)/3.14] = 4.9 feet or about 60 inches}

- L

- Stack height (feet)

Then,

12(60)1.20 × 50 = $81,646

{50 feet tall stack assumed for this example}

Motors and Fans

Using engineering judgment, an estimate of the cost of providing two fans and motors to power the capture hood and ventilation system and exhaust air from the filter house is made. More detailed cost estimating could be provided based upon fan type, duct runs, friction losses, pressure drop as well as motor types and energy curves and other considerations. However, the added effort required would probably not significantly improve the value of the overall cost estimating evaluation.

Then,

Motors & Fans = $50,000

An estimate of the auxiliary equipment cost is then the sum of these five values;

8,112 + 9,573 + 9,472 + 81,646 + 50,000 = $158,803

We now have enough information to complete a calculation of estimated total resource effectiveness for the add-on TSP control device. Using the template form for a Fabric Filter previously prepared, the source information collected from the facility’s ESDM and equipment costs estimated above, we may enter information into the form to complete the calculations. The Fabric Filter form contains typical values determined by USEPA based upon review of extensive cost information collected from installation of similar devices that are used to complete the estimate of the base equipment cost, direct and indirect installation costs and operating and maintenance costs. Ontario specific values have been included where appropriate to reflect costs associated with taxes, labor and utilities. Line-by-line review of the cost estimates by an environmental professional is necessary to establish the reasonableness of the estimates to the facility specific circumstances being evaluated.

Upon entering the Fabric Filter form, source information is entered to enable automated estimates of certain operating costs to be calculated. The source air flow (i.e. 57,000 acfm) and operating hours (i.e. 8,760 hours) are entered into the designated ‘boxes’ near the top of the form. Then values are added based on the calculations performed above to capture ‘Purchased Equipment Costs’, line a. ‘Control Device’ (i.e. $201,300) and line b. ‘Auxiliary Equipment’ (i.e. $158,803). Typical values for line c. ‘Instruments & Controls’, line d. ‘Sales taxes’, and line e. ‘Freight’ are automatically calculated.

Review of the default Purchased Equipment Cost values appears reasonable and they will be used. Instruments & controls have been estimated at 10% of combined control device and auxiliary equipment costs and reflect the cost of pressure and temperature monitors, perhaps a leak detection system, and VFD damper and motor controls. PST and GST taxes are estimated at 13% for Ontario and the cost of shipping control components from the manufacturing site to the installation facility is estimated at 5%. Freight is an obvious candidate for revision from the default value since shipping distance will directly and significantly affect cost. For this example the default value is accepted.

The Base Price (C) is automatically calculated by summing values from line a. through e.

Direct Installation Costs

Automated cost estimates continue to be calculated for Direct Installation Costs with typical values assigned as a ratio of the Base Price (C) determined for the purchased equipment. These represent costs directly associated with preparing, placing, connecting and otherwise installing the control device ready for operation. Typically, filter houses are installed on building roofs roughly above the source to be controlled if possible. Structural supports to hold the additional weight of the control system must be provided including platform, trusses, columns and foundations. These elements are estimated by line f. ‘Foundation’ at 4% of the base equipment price. This value could be significantly higher depending on site specific circumstances or lower if placing on the ground requiring only duct support and a concrete pad. The default value will be used for this example.

Line g. ‘Handling & Erection’ represents the bulk of the installation costs and represents staging, placing, connecting and installing all pollution control device related equipment. In this example, it is assumed that cranes would be used to lift structural members, duct work, stack, filter house, etc. to roof level for installation. Welding and bolting of components using skilled trades for rigging and welding etc. A typical cost estimate of 50% of the base equipment price appears reasonable for this example and has been used. Special circumstances can drive the cost higher such as needing helicopter lifts or staging to avoid production disruptions (lifting equipment over occupied building is generally not allowed).

Cost estimates for providing electrical connections including primary power supply and component wiring using skilled trade electricians is provided in line h. ‘Electrical’ and estimated at 8% of base equipment price. Site specific conditions could cause costs to be higher for this item such as the need for new transformers, switches or busses to provide power to the control device. This is not the case for the current example and the typical values will be used.

Plumbing and other pipe connections to the control system are estimated at 1% of the base equipment cost. Line i. ‘Piping’ includes cost associated with supplying water, compressed air and condensate drains required to make the TSP control system functional. Other costs such as natural gas piping and fire suppression could be included in this item for other control systems.

Thermal efficiency and condensation protection are important considerations for control systems especially in cold weather climates. Provision for ‘Insulation’ of air ducts and pipes is estimated at 7% of the base equipment cost in line j. The filter house is usually provided with insulation by the device supplier, but if required insulation is not provided then a cost estimate may be include in this line item. The typical fraction determined by USEPA will be used for this example.

Painting to provide corrosion protection and system durability is an important consideration. Line k. ‘Painting’ is provided to capture costs associated with application of functional coatings and is estimated at 4% of the base equipment cost. For this example, stainless steel has been specified for the filter house, air ducts and stack making painting of these elements unnecessary. However, painting of structural and support elements remain an important aspect to assure system durability and the 4% typical estimate does not appear to be excessive for this work and will be retained for the example.

Direct installation costs may involve activities that are completely unique to the site being evaluated and are therefore difficult to estimate using ‘typical’ factors obtained by comparing to similar installations. Items such as ‘Site Preparation’, ‘Facilities & Buildings’, and ‘Retrofit Costs’ should be considered by the environmental professional familiar with the site and installation requirements in estimating direct installation costs. Space is provided in the form (lines l, m & n) to include cost values as appropriate for these items.

Site preparation relates to the range of activities required to prepare the site for installation of the TSP control system and associated equipment. Site preparation could include ground clearing and leveling, building demolition, equipment removal, changes to existing roadways, parking, fencing and other existing features that must be rearranged to make access for the new equipment possible. For this example, it is assumed that no such site preparation is required.

Occasionally, installation of a control device involves the construction of new building(s) to house equipment. This could be in the form of a penthouse type structure erected on the roof of an existing building to provide weather protection for control equipment or a grade level building adjacent to the existing facility. Building is usually associated with larger, more extensive control systems. For this example, no building additions are projected.

Similarly, additional support facilities may be required to operate the control device. For the pulse jet type filters being evaluated in this example, compressed air is required to periodically remove particulate matter collected on the fiberglass filters. If the facilities capability to supply compressed air needs to be expanded (or provided) to accommodate the new equipment, then new ‘facilities’ must be added in the form of air compressor(s). Other control systems may involve handling waste water in terms of treatment and disposal. Still other control systems may involve handling special chemicals and hazardous waste that would involve additional ‘facilities’. All of these special ‘facility’ actions should be estimated and included in the direct installation cost. For this example, no special facility costs have been identified.

Additional site specific and unique requirements associated with ‘retrofitting’ control measures to existing facilities can add significant costs to installation. Provision is made in the form at line n. for ‘Retrofit Costs’. These are costs unique to the site and source that make installation more difficult and costly. Retrofit can be relatively difficult and subjective costs to estimate, but relate to things like space constraints, clearances and rearrangements required to install the equipment. Hoods, enclosures and ducts may be more difficult to place and existing equipment may need to be moved or changed to provide required access. Additional costs associated with retrofitting controls on existing equipment will almost always occur and can range from only a couple percent of the base equipment cost to as much as 1 or 2 times purchased equipment costs. Retrofit factors up to 50% of the base equipment cost are not unlikely and that is the amount used for this example.

In general, the larger and more complex the project, the greater the retrofit cost that should be expected. The environmental professional’s knowledge of the facility and equipment is critical in developing reasonable estimates for this cost element. Care should be taken to not double count costs. If extraordinary costs are projected for individual installation items such as additional structural steel, foundations, erection complexities, extra long duct, pipe and electrical runs, additional transformers, etc. in lines f. through m., then perhaps separately identified retrofit costs might be correspondingly lower. In addition, retrofit costs should not be thought of as contingency (those will be addressed separately). Retrofit costs should be anticipated and planned for while contingency costs would result from unanticipated events.

Total Direct Costs (DC) is then the summation of line items f. through n.

Indirect Installation costs

There are additional costs associated with installation of the TSP control system and result in indirect expenditures. The Fabric filter form automatically calculates values in line items o. through t. providing estimates for these indirect costs based upon typical rates determined by USEPA's survey of equipment suppliers and installations. For this example, the typical values will be used.

Line item o. ‘Engineering & Supervision’ represents the cost of system design and engineering supervision of field work. This item is estimated at 1% of the base equipment cost and appears reasonable. Line item p. ‘Construction & Field Expenses’ represents a kind of ‘catch-all’ for costs associated with getting the equipment installed and functioning. These include incidental costs related to construction and services, equipment and supplies obtained on-site to complete installation. Estimated at 20% of base equipment cost, it is accepted as a reasonable value for this example.

Contactor profit is reflected in line q. ‘Contractor Fees’ and is estimated at 10% of base equipment cost. Initial ‘Start-up’ is addressed at line r. and is estimated to be 1% of base equipment cost. Typically, equipment is not ‘turned over’ to the facility until operation consistent with the contract guarantee has been established. Start-up costs represent this initial trial operation. Closely related to start-up costs are ‘Performance Tests’ provided at line s. Initial performance tests are typically required to certify to the facility that TSP removal efficiencies are being achieved, as advertised. Other types of testing such as energy and pressure performance may also be specified. This item is estimated at 1% of base equipment cost. However, if system compliance testing is required to demonstrate to regulatory agencies performance levels achieved, then additional cost projections would likely be appropriate. The certification testing estimated for this example is $4,409. Compliance testing using approved test methods by independent professional services could cost $20,000 or more.

The last element of indirect installation cost estimating is to provide for unforeseen expenditures required to support completion of the project. A small estimate for ‘Contingencies’ of 3% of base equipment cost is provided at line t. for unanticipated occurrences such as labor disputes, stainless steel price increases, weather delays, etc.

The Total Indirect Costs (IC) is then determined by summation of line items o. through t.

Total Capital Cost (TCI) to purchase and install a pulse jet TSP filter system at the example facility is then estimated by the summation of Base Price (C), Total Direct Costs (DC) and Total Indirect Costs (TCI). The form automatically tallies the values.

The total capital cost represents a one-time investment in control technology over the life of the equipment. It is desirable to convert the total capital cost to equal annualized cost for the purpose of completing the evaluation of the total resource effectiveness of the potential control measure considered in this example. Using the amortization period of 10 years and interest rate of 6% provided in Section 2.5 of the Ministry’s GIASO document, the following multiplier is calculated.

i / {1 − (1 + i)-n}

Where,

- i

- 6 % interest rate

- n

- 10 year equipment life

Then,

0.06 / {1 − (1 + 0.06)-10} = 0.13587

The Capital Recovery Cost (CRC) is automatically calculated in the Fabric Filter form by multiplying Total Capital Costs (TCI) by the annualizing factor above.

Annual Operating and Maintenance (O&M) Cost

The example now proceeds to estimate costs associated with operating and maintaining the TSP control system. The Fabric Filter form automates many of the required cost estimates to simplify the calculations needed. The environmental professional performing the evaluation should review each line item to judge the reasonableness of the value for the specific source and site being considered. Similar to capital costs, operating O&M costs may be both direct and indirect.

Running the TSP control system requires personnel to start-up, shut-down and attend to the equipment during operation. Line a. ‘Operating Labor’ provides an estimate of cost based upon an hourly rate of $30/hour and an estimate that 2-hours per production shift is required to attend to the system. The 2-hour per shift estimate comes from USEPA survey of typical operating requirements for similar systems. Other estimates may be appropriate, but these values are judged to be reasonable for this example.

All operating personnel require supervision to schedule and direct activities. Line b. ‘Supervisor Labor’ provides and estimate for supervision as a faction (15%) of operating labor cost. The factor comes from USEPA's survey of similar TSP control systems and is accepted as reasonable for this example.

In addition to operating the TSP control system, maintenance also requires personnel. Line c. ‘Maintenance Labor’ provides an estimate of cost based upon an hourly rate of $40/hour and an estimate of 1-hour per production shift (on average) to maintain the equipment. Again, the time estimate comes from USEPA's survey of typical maintenance required for similar systems. Other estimates may be appropriate, but these values are judged to be reasonable for this example.

Routine maintenance usually involves the consumption of a variety of materials ranging from oil & grease, nuts & bolts and rags to hand tools such as wrenches and screw drivers. Line d. ‘Maintenance Materials’ is provided to estimate these costs and are typically considered to be about equivalent to the cost of maintenance labor.

Direct Labor Costs (DC) is then the summation of lines a. through d.

There are other direct operating costs in addition to labor. These are costs associated with maintaining spare parts, routine replacement parts/components, utilities, bulk material s, and waste disposal. The environmental professional must consider the potential POI reduction technique being evaluated and include the appropriate items in the cost estimate. For this example of a TSP control system it has been determined that replacement parts, compressed air and electricity would be required to operate the system. The Fabric Filter form identifies these items and provides automated estimates for the utilities to aid completion of the TRE calculation.

First, the form makes provision for ‘Replacement Parts’ at line e. and this is intended to reflect the need to periodically replace the fiberglass filters. For this example, it has been assumed that all the filters will need to be replaced every two years. Consequently, half the cost of providing all new fiberglass filters (see the initial equipment cost calculations above, Device Cost). Other estimates could be made, but this seems reasonable for typical fabric filter use.

Next, ‘Compressed Air’ is required to regularly ‘blow-off’ particulate matter accumulated on the filter surface. Provision for an estimate is provided at line f.

and an automatic calculation is provided in the Fabric Filter form based upon the following equation;

(air flow, cfm) × (operating hours) × 60 min/hr × 2 cfm pulse/1000 cfm air flow × $0.25/1000 cfm

Where,

- Air flow

- 57,000 cfm for this example

- Operating hours

- 8.760 hours per year for this example

- 2 cfm/1000 cfm air flow

- Typical air pulse required to remove particulate matter from filter surface

- $0.25/1000 cfm

- Typical cost to provide compressed air

Then,

57,000 × 8,760 × 60 × 2/1,000 × 0.25/1,000 = $14,980

Electricity is also required to power the TSP control system. An estimate of electricity required is provided at line g. ‘Electricity’ and an automatic calculation is performed in the Fabric filter form based upon the following equation;

(airflow, cfm) × (operating hours) × 3 hp/1000 cfm × 0.746 kWh/hp/$0.08/kWh

Where,

- Air flow

- 57,000 cfm for this example

- Operating hours

- 8.760 hours per year for this example

- 3 hp/1,000 cfm

- Typical power required to move 1,000 cfm of air

- 0.746 kWh/hp

- Conversion of power to energy

- $0.08/kWh

- Estimate of electricity cost in Ontario

Then,

57,000 × 8,760 × 3/1,000 × 0.746 × 0.08 = $59,599

There are other indirect operating costs that may not be immediately apparent but should be considered. Fortunately, there are typical factors that have been developed by USEPA based upon extensive review of similar control device installations that may be used to provide cost estimates.

‘Overhead’ at line h. allows for the cost associated with facility related organizational overhead to be provided. This has been estimated at 60% of Direct Labor Costs (D), is automatically calculated in the Fabric Filter form and has been accepted as reasonable for this example.

Non-facility or operational related costs such as sales & marketing, R&D, accounting, and other ‘home office’ type costs may be estimated at line i. ‘Administrate Charges’ and are automatically calculated in the Fabric Filter form using 2% of Total Capital Cost (TCI).

‘Property Taxes’, line j. and ‘Insurance’, line k. are both estimated at 1% of Total Capital Cost (TCI). Other values could be used, but these are considered representative for this example.