Transfer Payment Operational Policy 2020

This policy outlines the operational requirements and best practices that the Ontario government uses to support effective and proportional oversight of transfer payment activities.

This operational policy has been posted to help you better understand how decisions are made inside government and contains references to internal terms and applications used by Ontario government and agency staff.

1. Introduction

The Ontario Government provides transfer payments to recipients external to government to fund activities that benefit the public and are designed to achieve public policy objectives. The Transfer Payment Accountability Directive sets the administrative accountability framework for the oversight of these types of transfer payments.

Under the Transfer Payment Accountability Directive, transfer payments are provided to individuals (e.g. recipients of disability support payments), external organizations (e.g. public hospitals, school boards, not-for-profit corporations), or to other governments (e.g. municipalities).

Transfer payment oversight and accountability is also supported by financial management policies, which provide the direction and requirements for accounting, finance and controllership or/assurance of transfer payments (see appendix A for more information).

The Transfer Payment Operational Policy (Policy) is established under the authority of the Transfer Payment Accountability Directive, which authorizes the Secretary of Management Board of Cabinet to issue operational policies consistent with the Directive.

Where appropriate, sections from the Transfer Payment Accountability Directive are restated in this policy to provide context and clarity.

2. Effective date

This Policy is effective May 1, 2018.

3. Purpose

The purpose of this policy is to:

- set out operational requirements and best practices that support effective and proportional oversight of transfer payment activities;

- provide a consistent approach;

- be sustainable and forward-thinking to support and enable strategic priorities; and

- support productive relationships with transfer payment recipients.

4. Application and scope

This policy applies to:

- ministries; and

- provincial agencies that have a mandate to provide transfer payments.

Unless otherwise stated, for the purpose of this policy, the term "ministry" includes both ministries and provincial agencies.

As set out in the Transfer Payment Accountability Directive, organizations and individuals who receive transfer payments are referred to as "transfer payment recipients".

For clarity, both the Transfer Payment Accountability Directive and this policy apply only to the subset of transfer payments that fund activities for a specific purpose - to benefit the public, and to achieve public policy objectives. The Directive and this policy do not apply to any other types of transfer payments (e.g. transfer payments provided to provincial agencies).

The Directive sets out three types of payments. This Policy applies to two of these: time-limited payments and ongoing payments. It does not apply to support payments.

In addition to the requirements outlined in this Policy, ministries must comply with all relevant corporate directives and policies relating to the oversight of transfer payment activities, including policies and guidelines issued by the Office of the Provincial Controller Division, which are available on the Ontario Public Service Financial Management Gateway.

Where a conflict or inconsistency occurs between any of the requirements outlined in this policy and those specified in any legislation or regulation pertaining to the administration of a named transfer payment activity and/or its recipients, this policy is subordinate to those requirements.

5. Principles

The Transfer Payment Accountability Directive establishes a set of principles to guide the application of the Directive. Those principles focus on: accountability; value for money; risk-based approach; fairness; integrity and transparency; focus on outcomes; common processes; information collection and sharing; and communication.

This policy establishes an additional six principles to further guide transfer payment relationships and the administration of transfer payment agreements.

Operational policy principles

Guiding principles for creating transfer payment relationships

- Stewardship: Public resources produce best value where expected outcomes are clearly defined, and programs and organizations are focused on enabling and achieving those outcomes.

- Reciprocal respect: A transfer payment is the result of a partnership based on reciprocal respect.

- Accountability: Parties to a transfer payment agreement must be accountable for addressing expected outcomes. Good administration supports accountability by providing transparency and capacity to deliver.

Guiding principles for administering transfer payments

- Simple: Processes are streamlined and digitized, definitions and templates are standardized, and language is concise and clear to support clear communication and common understanding. Information is only requested when there is a plan to use it.

- Proportional: Application processes, reporting and other requirements are reasonable and proportional to the value of the funding and risk profile of the funding arrangement.

- Flexible: Budget flexibility allows transfer payment recipients to adjust and innovate to deliver expected outcomes and meet community needs within appropriate and transparent financial guidelines.

6. Requirements and best practices

This policy sets out requirements and best practices for assessing risk for mandatory registration for transfer payment recipients; agreements; and proportional oversight.

Compliance with this policy’s requirements is mandatory.

The inclusion of best practices in this policy is intended to profile practices that have demonstrated success and to promote modernization efforts. While compliance with best practices is not mandatory, ministries are strongly encouraged to incorporate best practices into their transfer payment management and oversight activities, where appropriate.

6.1 Enterprise transfer payment systems

Section 6.1 of this policy applies only to ministries and does not apply to provincial agencies

The Transfer Payment Ontario (TPON) system is the enterprise system for managing time-limited and ongoing transfer payment activities.

TPON is an online case-management system that helps ministries manage the lifecycle of transfer payment programs. TPON is also integrated with the Integrated Financial Information System (IFIS).

TPON includes a central repository of recipient information. Ministries use this information to support their transfer payment management and oversight activities, and this Policy includes requirements related to these activities.

Registration Requirements

- Ministries must inform recipients that are applying for transfer payment funding, or are in receipt of transfer payment funding, that registering and validating their organizational information in TPON is mandatory.

- Ministries must ensure a recipient’s registration has been completed in TPON before entering into an agreement, renewing or making changes to an existing agreement.

- Ministries must use the data from TPON as the authoritative source for recipient organizational information. This means that ministries must first check TPON to verify if the information is available and up-to-date before requesting it directly from the recipient.

The Ministry of Government and Consumer Services manages the TPON system. For more information on TPON, refer to Transfer Payment Ontario on InsideOPS.

6.2 Agreements

6.2.1 Electronic agreements and signatures

The use of electronic agreements and signatures can improve administrative efficiency and is environmentally sound. This section provides requirements for ministries proceeding with electronic administration of new, renewed, renegotiated or amended transfer payment agreements.

Requirements

- Ministries must discuss the use of electronic formats for agreements and signatures with their transfer payment recipients. If a recipient agrees to the use of electronic administration for transfer payment agreements:

- Ministries, in consultation with their legal counsel, must determine the standards, rules and other requirements necessary to manage the risks associated with the use of electronic agreements and signatures.

- Ministries must provide the transfer payment agreement in an electronic format, and must accept signed transfer payment agreements from the recipient in an electronic format as an authoritative source.

- When accepting signed transfer payment agreements in an electronic format, ministries must confirm that the content has not been modified in any way and the agreements have been signed by the appropriate signing authority. An example of an acceptable verification process is that the signed agreement must be sent from the signing authority’s email account, or another agreed upon email account.

- In all cases, ministries must comply with the Accessibility for Ontarians with Disabilities Act, 2005 (AODA) requirements, and respond to requests for accessible agreement formats and communication formats in a timely manner at no extra cost to the recipient.

6.2.2 Amendments and updates to agreements

Agreements may need to be updated from time to time to respond to changing circumstances. This section provides direction on amending existing agreements.

Requirements

- Ministries must consult with their legal counsel on any proposed amendments to transfer payment agreements prior to making any changes.

- Circumstances in which ministries must update or amend transfer payment agreements include, but are not limited to:

- Any legislative or regulatory requirements imposed on the transfer payment activity or transfer payment recipient since the agreement was originally signed.

- The risk profile of the recipient and/or the risk of the transfer payment activity changes as a result of a risk assessment.

- Funding and/or service/activity levels change.

- Change to ministry or government priorities that would affect an existing transfer payment agreement.

- Ministries must provide the transfer payment recipient with information about any amendments to the agreement.

Best practice

- Ministries should notify transfer payment recipients in advance of any amendments or updates to transfer payment agreements. A minimum of 30 days advance notification is recommended.

6.2.3 Right To Audit and Record Keeping

This section provides direction that requires that all transfer payment agreements contain terms and conditions that establish and support the Ontario government’s right to audit.

Requirements

- Ministries must consult with their legal counsel on any new agreements and on any proposed amendments to agreements prior to making any changes.

- Ministries must ensure that each agreement includes terms and conditions that provide the Ontario government with the right to audit the recipient with respect to the transfer payment.

This requirement is satisfied in the following situations:

- The ministry uses the standard Transfer Payment Agreement Template, which contains terms and conditions that establish a right to audit and record keeping requirements.

- The ministry uses the right to audit clause and record keeping requirements from the standard Transfer Payment Agreement Template in a transfer payment agreement.

- In consultation with legal counsel, the ministry develops an appropriate right to audit clause and record keeping requirements that provide the Ontario government with the right to audit the recipient with respect to the transfer payment.

- In consultation with legal counsel, a right to audit clause is deemed to be part of an agreement if there is statutory authority that sets out the right to audit.

Best practice

- Where appropriate, it is recommended that ministries use the standard Transfer Payment Agreement Template, which includes comprehensive record-keeping and audit provisions. The template can be found on the Corporate Directives and Policies site on InsideOPS.

6.3 Proportional oversight

Oversight approaches, such as reporting requirements, must be proportional to the assessed risks. This means that if the recipient and activity risks are low, ministries have the opportunity to assess such risks and adjust the ministry’s level of oversight of the activity and recipient accordingly. Similarly, if the outcome of the risk assessment is high for the recipient and activity, ministries may exercise greater oversight.

Direction on risk assessment for transfer payment recipients and activities is provided in three key instruments:

- OPS Enterprise Risk Management Framework;

- Risk Management Guidance - Transfer Payment Accountability Directive; and

- Transfer Payments Financial Management Policy.

The Transfer Payment Financial Management Policy requires ministries to consult the Transfer Payment Recipient Report (formerly known as the Financial Insight Report or FIR) and consider the full funding relationship the Province has with a transfer payment recipient before providing transfer payment funding.

For more information on risk assessments, see appendix A.

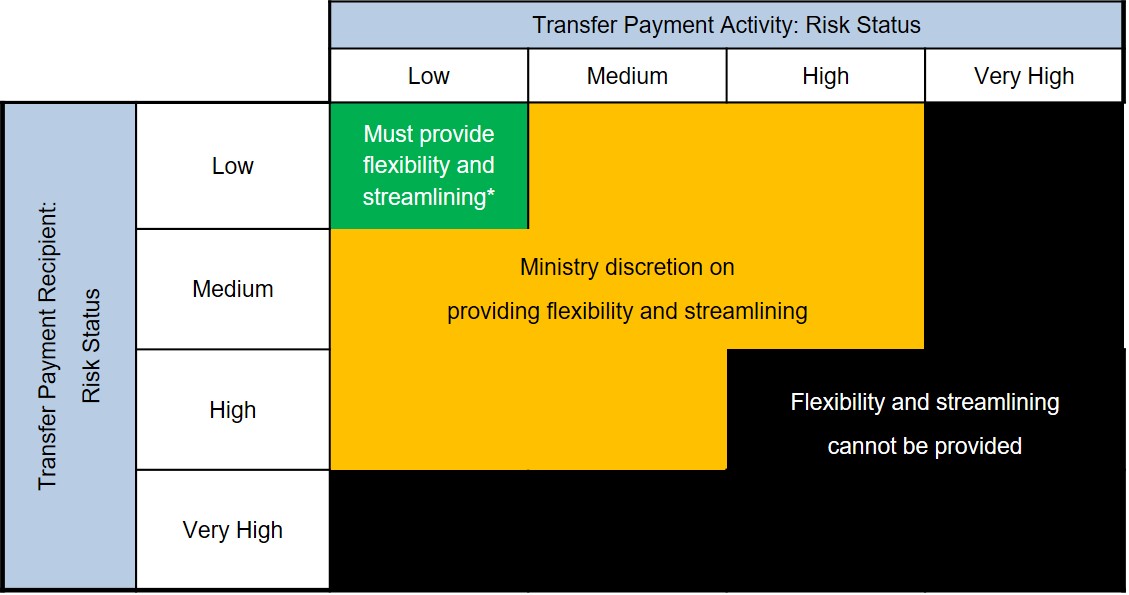

6.3.1. Risk assessment matrix and general approach

The following matrix is a tool to support ministries in their assessment of transfer payment recipient and activity risks. The outcome of the risk assessment will assist ministries in determining whether flexibility and streamlining approaches could be provided.

* The three flexibility and streamlining approaches set out in this policy are:

- budget flexibility

- streamlined reporting

- streamlined agreement renewal

While this policy sets out these three approaches, there may be other approaches that ministries can also employ to effectively exercise proportional oversight where the risk is low.

Excluded situations

Notwithstanding the requirements below, ministries may choose not to provide the three flexibility and streamlining approaches or any other approaches to support streamlining, in the following situations:

- Where legislative or regulatory requirements exist that conflict with or are inconsistent with this policy (e.g. legislation that requires first quarter reports); or

- Where program requirements conflict with or are inconsistent with this policy.

Pre-requisite

- Ministries must ensure that transfer payment recipient and activity risk assessment ratings are current.

- Ministries that have decided to provide flexibility and streamlining must consult their legal counsel to ensure that the transfer payment agreement contains terms and conditions to support the specific flexibility and streamlining approaches that the ministry has decided to provide.

Requirements

- Ministries must assess whether the flexibility and streamlining approaches are appropriate for all new, renewed and renegotiated transfer payment agreements.

- Where both the transfer payment recipient risk and activity risk is low (see matrix above), ministries must provide the flexibility and streamlining approaches, unless one of the excluded situations in section 6.3.1 apply.

- Ministries must not provide the flexibility and streamlining approaches if the assessed risk is such that the approaches cannot be provided (see matrix above).

- Ministries must review the application of the flexibility and streamlining approaches and make appropriate adjustments if either or both the recipient or activity risk levels change.

- Ministries must carry out the flexibility and streamlining approaches in accordance with the terms of the applicable transfer payment agreement.

- Ministries must document both the risk assessment process and the decision made for providing the flexibility and streamlining approaches to transfer payment recipients.

Best practice

- Ministries should consider providing the flexibility and streamlining approaches to recipients when they are not renegotiating or renewing existing transfer payment agreements, if appropriate.

6.3.2 Budget flexibility

Budget flexibility is the ability for a transfer payment recipient to re-allocate certain funds between designated expenditure categories without the prior approval of the ministry.

Up to 10 per cent of the funding per transfer payment activity is available for budget flexibility.

Requirements

- Ministries must provide budget flexibility where both the recipient risk and the activity risk is low (see matrix above), unless one of the excluded situations in section 6.3.1 apply.

- Ministries must not provide budget flexibility if the assessed risk is such that the flexibility and streamlining approaches are not available (see matrix above).

- Re-allocation must be within the same transfer payment activity within one fiscal year, or within the agreement funding period. For multi-year agreements, re-allocation must be within the authorized spending level in each fiscal year.

- Ministries must verify that recipients apply budget flexibility within the following parameters:

- Re-allocation of funds must be within the same Executive Control, as defined in the Expenditure Management Directive

- Re-allocation of funds must not be used for administrative costs or "other" costs, as per Ministry definition

- Ministries must require transfer payment recipients to identify the re-allocated funds, including the rationale for re-allocation, in their next financial reporting process or more frequently if requested by the funding ministry.

- Ministries must undertake a process of corrective action(s) in a timely manner in the event that transfer payment recipients have inappropriately re-allocated funds.

- Under exceptional circumstances, ministries may provide budget flexibility in excess of 10 per cent. In such cases, ministries must develop a business case and receive the appropriate approval prior to providing budget flexibility (see Appendix B for business case and approval criteria).

Best practice

- If a ministry determines as a result of its risk assessments that the risk status of either a transfer payment recipient or activity falls within the ministry’s discretion, the ministry should consider whether budget flexibility can be provided (see matrix above).

6.3.3 Streamlined reporting

Reporting is a necessary oversight mechanism. Appropriate reporting provides meaningful information and supports accountability. The reporting requirements imposed by a funding ministry should be in proportion to the assessed recipient and activity risk. By conducting risk assessments periodically, ministries can review reporting requirements and consider whether they are appropriate and where they can be streamlined.

When determining reporting requirements, ministries should consider the following:

- Is there information being requested that is not used?

- Are there opportunities to consolidate requests with other funding ministries or to share information?

Requirements

- Ministries must remove any requirements for a first quarter financial report (or first financial report), where both the recipient risk and the activity risk is low (see matrix above), unless one of the excluded situations in section 6.3.1 apply.

- Ministries must ensure that reporting frequency is appropriate and necessary.

- Within the same ministry, program areas funding the same recipient must investigate opportunities to streamline and consolidate reporting (such as the use of the Standard Multi-Project Agreement Template or consolidating year-end reconciliation for a multi-funded recipient). Where opportunities are identified, ministries must consolidate and streamline reporting.

Best practices

- If a ministry determines as a result of its risk assessments that the risk status of either a transfer payment recipient or activity falls within the ministry’s discretion, the ministry should consider whether streamlined reporting can be provided (see matrix above).

- Program areas in different ministries funding the same recipient for a similar activity should work together to identify opportunities to streamline and consolidate reporting. Such opportunities could include implementing common reporting requirements, setting out such requirements in a common agreement such as the Standard Multi Project Agreement Template, consolidating year-end reconciliation, or aligning the timing for recipient reporting.

6.3.4 Streamlined agreement renewal

A streamlined agreement renewal process is intended to eliminate negotiations at the time of agreement renewals where there is no value or benefit to the ministry or transfer payment recipient in undertaking such negotiations. It can be provided when there are no changes required from one agreement funding period to the next, including any changes to the funding amount and any transfer payment recipient obligations under the agreement.

Payments continue to be subject to the same financial rules (Cash Management Directive, Financial Management Policy etc.).

Requirements

- Ministries must provide a streamlined agreement renewal process where both the recipient risk and the activity risk are low (see matrix above), unless one of the excluded situations in section 6.3.1 apply.

Best practice

- If a ministry determines as a result of its risk assessments that the risk status of either a transfer payment recipient or activity falls within the ministry’s discretion, the ministry should consider whether streamlined agreement renewal can be provided (see matrix above).

7. Definitions

All of the following definitions, with the exception of Authorized Spending Level, Risk Management Process and Transfer Payment Agreement, have been taken from the Transfer Payment Accountability Directive. Inclusion of these definitions in this policy is for ease of reference.

Authorized spending level

An authorized spending level is the maximum amount of expenditures that a transfer payment recipient can incur against a transfer payment activity for a given fiscal year.

Canada Revenue Agency (CRA) business number

The CRA business number is a nine-digit identifier for businesses to simplify their dealings with federal, provincial, and municipal governments in Canada. It aims to give each registered business its own unique number.

Provincial agency

A provincial agency is an entity that is subject to the requirements of the Agencies and Appointments Directive.

Risk

The effect of uncertainty on objectives. It can be characterized as either a potential negative or positive consequence or event that deviates from an expected output or outcome.

Risk assessment

The method used to determine risk management priorities by evaluating and comparing the level of risk against pre-determined standards, target risk levels or other criteria.

Risk management

A systematic approach to setting the best course of action under uncertainty by identifying, assessing, understanding, acting on, monitoring, and communicating risk issues.

Risk management process

A systematic decision and management tool that consist of a five-stage cycle: clarify objectives, identify risk, assess (measure) risk, plan and take action to manage risk, and monitor risk.

Transfer payment

Transfer payments are a mechanism used by the Ontario government to fund activities that benefit the public and are designed to achieve public policy objectives. Transfer payments are transfers of money to individuals (e.g., recipients of disability support payments), external organizations (e.g., public hospitals, school boards, not-for-profit corporations) or to other governments (e.g., municipalities, First Nations) for which the Ontario government does not:

- Receive goods or services directly in return, as would occur in a purchase or sales transaction

- Expect to be repaid in the future, as would be expected in a loan

- Expect a direct financial return, as would be expected in an investment.

Transfer payment activity

An activity, funded via a transfer payment, that has a clear purpose, supports a ministry program, and is connected to the achievement of a public policy objective.

Transfer payment agreement

A signed document required for the management and oversights of all transfer payment activities, that clearly identifies the rights, responsibilities and obligations for both the recipient and the accountable ministry. Ministries must have a signed agreement in place with a recipient before a transfer payment is provided.

Transfer payment recipient

An individual or entity that is legally capable of contracting (e.g., a corporation) that has received a transfer payment from the Ontario government.

Appendix A: Information on risk assessments

The OPS Enterprise Risk Management Framework requires ministries and agencies to establish and maintain an effective system of risk management and to integrate risk management practices into all levels of the organization.

The Risk Management Guidance - Transfer Payment Accountability Directive outlines how risk management concepts and practices can be applied to conduct a risk assessment and develop a risk management plan to support a proportional, risk-based approach to the oversight of transfer payments.

The Transfer Payment Financial Management Policy sets out information and rules on the use of the Transfer Payment Recipient Report (formerly known as Financial Insight Report or FIR). The policy requires ministries to consult the Transfer Payment Recipient Report and contact previous funders prior to providing transfer payment funding to a recipient.

Appendix B: Business case criteria for exceeding budget flexibility rate

When seeking to provide budget flexibility in excess of 10 per cent, the ministry must bring forward a business case setting out the rationale for the increased flexibility.

Approver

Ministries: Chief Administrative Officer (CAO)

Provincial Agencies: CAO equivalent (e.g. Chief Financial Officer)

The business case, or rationale, must include, at minimum, the following information:

- The specific approval being sought

- Rationale for exceeding the 10 per cent budget flexibility, including information on the current risk assessment

- Current ministry process/approach to budget flexibility, including addressing any issues with consistency for other transfer payment recipients that the ministry funds

- Risk assessment of proceeding and of not proceeding, and any mitigation strategies

- Any other options considered to support proportional oversight

- Identification of any public/media interest related to the transfer payment recipient and the activity

- Any amendments to the transfer payment agreement that might be necessary (note that consultation with legal counsel is required)

- Any other information that maybe relevant for decision maker