Provincial Wood Supply Strategy

A consolidated wood supply report and plan of action. The primary purpose is to identify critical wood supply issues and provide strategies to address those issues.

Provincial wood supply strategy

Forest policy series

A digital copy of this publication is available at no charge by emailing the Manager, Timber Allocation and Licencing Section in Forest Industry Division.

Telephone inquiries about ministry programs and services should be directed to the Natural Resources Information and Support Centre:

General inquiry

Fax

Executive summary

This document presents a picture of the wood supply and a set of strategies for the Province of Ontario. It was produced by the Ministry of Natural Resources (MNR) with input from key stakeholders. The primary purpose of the Provincial Wood Supply Strategy is to identify critical wood supply issues and provide approaches (strategies) for addressing those issues.

There are two primary objectives focused on sustaining wood supply within the bounds of overall forest sustainability:

- To sustain a continuous, predictable, long-term wood supply necessary for industrial processing facilities; and,

- To increase the level of long-term available wood supply.

The Provincial Wood Supply Strategy responds to legal commitments described in Condition 48 of the Declaration Order Regarding MNR’s Class Environmental Assessment Approval for Forest Management on Crown Lands in Ontario (MNR-71) as released in June 2003. This strategy document also supports the MNR vision of sustainable development and mission of ecological sustainability. The Crown Forest Sustainability Act states that Crown forests are managed to meet social, economic and environmental needs of present and future generations. This document replaces in whole the Regional Wood Supply Strategies, published by the MNR in 2003.

This strategy document is provincial in scope. Each of the three MNR administrative regions has a separate section to provide a regional context and a discussion of regional scale issues. The significant issues and related strategies are identified within the area of the Boreal and Great Lakes-St. Lawrence Forest regions. The strategies themselves will be implemented at the provincial, regional and/or local management unit level. The scope and implementation is described within the discussion for each of the strategies.

The Provincial Wood Supply Strategy is linked directly to the Ontario Forest Accord and the Ontario Forest Accord Advisory Board’s (OFAAB) proposal for “Room to Grow.” The OFAAB recommended in its final report that the regional wood supply strategies serve as the instrument for benchmarking the long-term wood supply available to Ontario’s forest industry and for identifying the threshold that would initiate “Room to Grow” sharing discussions. Appendix 1 contains the utilization benchmarks necessary to facilitate this process.

The foundation for this strategy document is the wood supply database contained in Appendix 1. This database graphically presents wood supply, demand and utilization information for each management unit and species group. The information is then aggregated into regional and provincial graphs of wood supply and demand. Part 2 of this strategy document examines wood supply and demand in a regional context. The analysis was conducted to determine the ability of the Crown forests to continue to supply Ontario’s forest industry into the future, and to identify wood supply issues. No attempt was made to forecast future demand levels, or to predict future trends in the forest products sector. The dynamic nature of the forest industry is purposefully outside the scope of this wood supply strategy.

Part 3 is the essence of the document. It contains the significant issues and the strategies recommended to address those issues.

Boreal Forest Issues and Strategies

Following an analysis of the data and an examination of the forest management context, two issues were identified in the Boreal Forest:

- Future wood supply drops below current demand; and,

- Quality of wood supply information.

These two issues are also relevant to the Great Lakes-St. Lawrence Forest although the context is different. Hence, the strategies addressing these issues are provincial in scope.

Across the Boreal Forest, wood supply is predicted to fall below the level of industrial demand in the near future. The wood supply gap, which has been forecast for many years, is primarily the result of an age-class imbalance in the forest itself, but this situation has been compounded by a number of other factors.

The forecast for the two administrative regions within the Boreal Forest predicts that the spruce-pine-fir (SPF) supply will fall below the demand level in 5 to 10 years and take 80 years to fully recover. For poplar, the forecast is for supply to fall below demand in 15 years, with recovery in about 70 years. The supply gap is by far the most critical issue facing the forest industry in this part of the Province. The developing gap between wood supply and demand presents an unavoidable dilemma – increase the wood supply or reduce mill consumption.

The second issue applies across the entire province. The ability to accurately predict wood supply is limited by the quality of the information on which we base wood supply projections within forest management planning. The quality of information is strongly tied to the issue of wood supply. Information quality affects wood supply from two perspectives. First, better information increases confidence in the conclusions regarding the nature and degree of the wood supply gap. Second, more reliable information allows forest managers to make decisions which optimize the management and use of forest resources. For example, more accurate resource inventory and increased knowledge of forest succession will allow for improved decisions concerning the scheduling of forest stands for harvesting.

Eleven strategies are proposed to help mitigate these two issues within both the Boreal Forest and the Great Lakes-St. Lawrence Forest. They are:

- Review the wood demand for mills;

- Provide demand information to planning teams to help set appropriate plan objectives for wood supply;

- Promote best practices for forest management modelling;

- Improve growth and yield information;

- Improve forest resources inventory;

- Improve the knowledge of stand condition and forest succession;

- Increase utilization of available wood:

- Use silviculture to increase forest productivity;

- Monitor the effectiveness of silvicultural treatments;

- Implement a fire management strategy for Ontario; and,

- Ensure guide effectiveness and efficiency.

Great Lakes-St. Lawrence forest issues and strategies

Five wood supply issues were identified as significant and particular to the Great Lakes-St. Lawrence Forest:

- Current shortage of high-quality sawlogs and veneer in the region;

- Long-standing surplus of low-grade hardwoods;

- Sustainability of the private land harvest;

- Long-term regional trend towards declining poplar supplies; and,

- Regeneration problems in older white pine shelterwood treatments.

Strategies 1 to 11 for the Boreal Forest, which address the issues of long-term wood supply and the quality of information, also pertain to the Great Lakes-St. Lawrence Forest.

There are nine additional strategies which pertain specifically to the Great Lakes-St. Lawrence Forest:

- Continue efforts to improve the growing stock after harvest through proper tree marking and stand improvement practices;

- Continue efforts to minimize logging damage to residual trees;

- Study methods to minimize logging damage done by mechanized harvesting;

- Salvage high-quality trees with high mortality risk during tree marking;

- Maximize the harvest of available pulpwood;

- Give support for permits to export tolerant hardwood pulpwood;

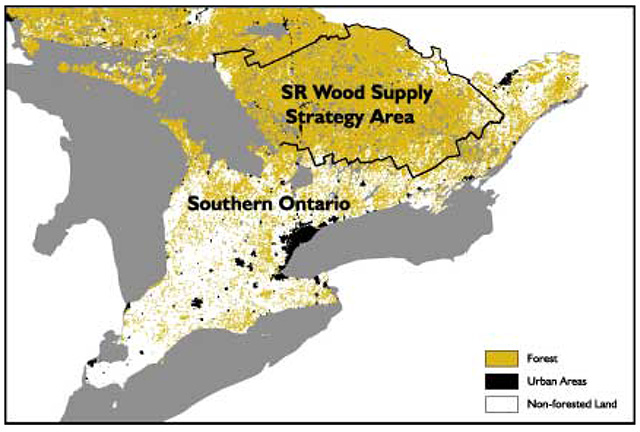

- Conduct a private land wood supply study within Southern Region;

- Advise poplar using industries of the forecasted declining poplar supply; and,

- Ensure that past white pine shelterwood treatments are regenerated in accordance with the requirements of their licence.

The Provincial Wood Supply Strategy and the strategies contained herein are not meant to be prescriptive. The intent of this initiative is to provide information and a suite of tools to help manage wood supply issues to meet future needs. When implemented, the strategies will move forest management towards a secure, predictable supply of wood for industry and the potential of surplus for additional parks and protected areas.

Purpose, objectives, and principles

Purpose

Produced by the Ministry of Natural Resources (MNR), this document presents a consolidated wood supply strategy for the Province of Ontario.

The purposes of this document are to:

- Document industrial wood supply and demand;

- Document the benchmark of the long-term supply for sharing under “Room to Grow”;

- Identify critical wood supply issues;

- Provide strategies to address the identified issues; and,

- Fulfill the legal commitment under Condition 48 of the EA Approval for Forest Management.

footnote 2

Strategy objectives

The Provincial Wood Supply Strategy initiative supports two primary objectives:

- To sustain a continuous, predictable, long-term wood supply necessary for industrial processing facilities; and

- To increase the level of long-term available wood supply.

These two objectives are achieved only within the bounds of overall forest sustainability as defined by the Crown Forest Sustainability Act and as determined at the local level through the forest management planning process.

Strategy principles

The appropriate context and direction for addressing wood supply issues is defined by a set of principles. The development and implementation of strategies to achieve the wood supply objectives will be guided by these principles:

- Wood supply is determined at the local level through the forest management planning process and is an outcome of planning for a broad set of economic, social and environmental objectives. This planning process requires the appropriate application of all forest management guides;

- Future investment by the forest industry and its ongoing contribution to the provincial economy is highly dependent on the quantity, quality and cost of wood supply;

- The present and future economic and social vitality of many communities in northern and central Ontario is dependent upon the quantity, quality and cost of wood supply;

- Strategies that increase wood supply have the potential to secure and increase community benefits and employment;

- The impact of the quantity and quality of wood supply on the social and economic vitality of local communities is described and assessed during the development and approval of forest management plans;

- Strategies are designed to support the Ontario Forest Accord and the “Room to Grow” policy framework;

- Permanent increases in wood supply will enable sharing between industrial use and protected areas establishment in accordance with the “Room to Grow” policy framework;

- Estimates of wood supply need to be based on sound resource inventory and scientific information (high quality natural resource science and information) in order to ensure sound decision-making related to forest sustainability and the availability of fibre for industrial processing; and

- Estimates of wood supply and the effect of the various factors affecting wood supply need to be monitored and publicly reported to facilitate adaptive management and accountability.

Part 1. introduction

Wood supply and forest sustainability

Ontario’s forests are managed for a broad range of uses and to conserve economic, social, environmental and cultural values. Sustainable development is the vision of the Ministry of Natural Resources.

The mission of the Ministry of Natural Resources is to manage our natural resources in an ecologically sustainable way to ensure they are available for the enjoyment and use of future generations. Ecological sustainability focuses on safeguarding the province’s natural capital and nature’s capacity to renew itself. To achieve sustainability, forest ecosystems must be maintained in a healthy state, and the value of the forest to all users must be respected.

Although this document is aimed at ensuring that “current demand” for wood for the forest industry is given appropriate consideration during the forest management planning processes, the principle of forest sustainability is at its core. The estimates of supply are those of existing approved forest management plans, all of which are based on long- term forest sustainability. Wood supply is determined through the forest management planning process, at the local level, as an outcome for planning for a broad set of economic, social and environmental objectives. None of the strategies can supersede or contravene any provision of the Crown Forest Sustainability Act. Consequently, they are limited to addressing wood supply issues within the parameters of forest sustainability as defined by the Act and its regulations.

Policy context

In Ontario, the Ministry of Natural Resources is the steward of Crown lands, waters and natural resources. Most of Ontario’s forests (82 percent) are owned by the Crown. Provincial commitments and responsibilities for the sustainable management of Ontario’s Crown lands and resources are expressed in the MNR vision, mission, broad objectives and desired outcomes.

The Policy Framework for Sustainable Forests (MNR 1994) provides the overall direction for an ecosystem-based approach to the management of Ontario’s Crown forests. The ministry’s commitment to forest sustainability is provided through Ontario’s key forest act – the Crown Forest Sustainability Act (CFSA). The CFSA requires that forest management plans be prepared for each designated management unit in accordance with the Forest Management Planning Manual, which is one of four regulated manuals under the CFSA. A forest management plan describes the forest management objectives and strategies applicable to the management unit while having regard to the plant life, animal life, water, soil, air, and social and economic values, including the recreational values and heritage values of the management unit. It is developed at the local level in an open and consultative fashion with the assistance of an interdisciplinary planning team and a local citizens committee. Direction for the writing of a forest management plan is also provided by a variety of guides and policies.

The Provincial Wood Supply Strategy responds to Condition #48 as set out in the Declaration Order Regarding MNR’s Class Environmental Assessment Approval for Forest Management on Crown Lands in Ontario (MNR-71). MNR worked directly with the forest industry and environmental non- governmental organizations during the development of this strategy. The Provincial Forest Policy Committee was also consulted and made recommendations on the development process.

The Forest Resource Assessment Policy (2003), commonly referred to as FRAP.

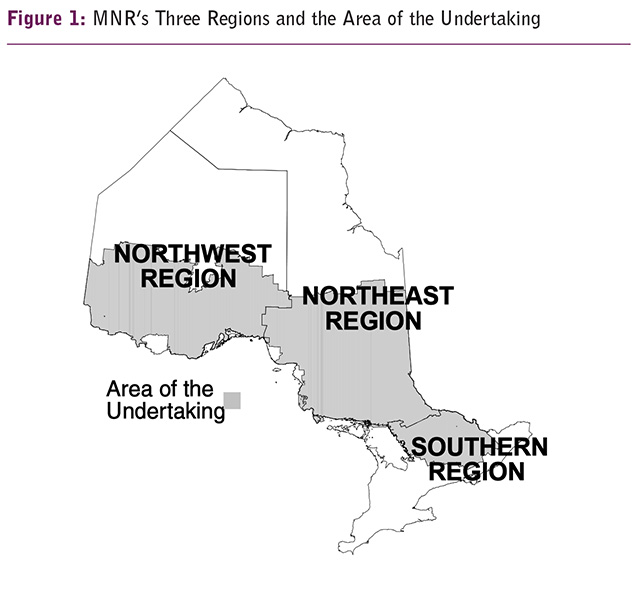

Figure 1: MNR’s Three Regions and the Area of the Undertaking

As indicated earlier in this document, the objectives of the Provincial Wood Supply Strategy are to sustain and, where possible, permanently increase wood supply for both industrial use and opportunities to grow parks and protected areas. The proposed policy framework for “Room to Grow” is a separate initiative which is linked to the Provincial Wood Supply Strategy. It is discussed in detail later in this section.

Two other initiatives with implications for the supply of wood to forest industry are currently under development. First, the Forest Sector Strategy is examining the potential impact that various large-scale and long-term influences will have on the commercial forest sector in Ontario. The objective of this project is to develop strategies and tactics to address the broader economic, commercial and social challenges and opportunities that will face the forest sector in the coming years. It will have a much broader scope than the Provincial Wood Supply Strategy.

The second initiative with implications for industrial wood supply is the Enhanced Forest Management – Science Information and Analysis initiative of the Provincial Forest Policy Committee. This project will focus on establishing a source of dedicated, long-term funding that will assist the government and the forest industry in better understanding silviculture effects and effectiveness (on growth and yield, environment, etc.) in order to maximize returns on silviculture investments. Action on this project will assist with the implementation of the strategies contained within this document.

Implementation of strategies

This initiative brings Ontario’s wood supply and demand information into one framework document, together with strategies for addressing challenges and capitalizing on opportunities. Specifically, the regional reports compare the supply forecasts from approved forest management plans against the current level of industrial demand in order to identify potential shortages and surpluses. Part 3 identifies the major wood supply issues, both current and forecast, and recommends strategies to manage them.

The wood supply strategies contained in this document will be implemented through normal channels, either as a part of the production and approval of forest management plans or through existing CFSA mechanisms. The strategies are in the form of recommendations to be considered during forest management planning, mill benchmarking exercises, licensing processes, research priority setting, or during the development of MNR or company policy. At the management unit level, appropriate strategies must be considered for inclusion in a forest management plan early in the planning process when wood supply issues are anticipated.

These represent MNR wood supply strategies and do not necessarily reflect those of any one community or forest company. Each company looks at its own supply picture and develops its own supply strategies. These strategies look at the bigger picture of wood supply across an entire region and not just one mill, one management unit or one company woodshed.

MNR holds responsibility for the stewardship of Ontario’s natural resources.

Although the management of Crown forests in Ontario is the responsibility of the provincial government, the majority of planning and forest management activities are carried out by the forest industry under licensing arrangements, on behalf of the Crown. Most of the strategies contained in this document will therefore be carried out by the forest industry or with the cooperation of industry. MNR will work with the forest industry to generate cooperative approaches to implementing the strategies. Some strategies will be implemented directly within the existing processes, such as forest management planning. Other strategies will require the development of new processes or partnerships for implementation. Many of the strategies will require collaborative efforts between MNR and forest stakeholders in a spirit of mutual benefit.

Most of the strategies will be implemented “on the ground” at a management unit or woodshed level. However, many of the strategies will be coordinated at a broader level – at the region or province – since the scope of the strategy is normally broader than the local area. As an example, local yield tables will be applied within a forest management plan, but the collection of information by MNR and the forest industry will be coordinated from the regional or provincial level. The scale of implementation and scope is described within each strategy.

While the wood supply strategies contained in this document are to be reviewed and revised periodically (as required by MNR’s Class EA for Forest Management), they may be revised at any time if an important wood supply issue arises. The supporting data are to be updated annually, as new management plans are approved and as existing Ministry Recognized Operating Levels (MROLs) are amended. A summary of the current Provincial Wood Supply Strategy will be provided in each five- year Environmental Assessment report.

The Ontario Forest Accord and Room to Grow Policy Framework

As mentioned above, the Provincial Wood Supply Strategy is directly linked to the Ontario Forest Accord and the Ontario Forest Accord Advisory Board’s (OFAAB) recommended “Room to Grow” policy framework. It is the Provincial Wood Supply Strategy that documents the harvest data and supply forecasts as well as the OFAAB benchmark, Table 1. The benchmark is an essential part of the data required for “Room to Grow” discussions.

The Ontario Forest Accord is an historic agreement signed in 1999 that resulted in the addition of 378 new parks and conservation reserves totaling 2.4 million hectares to Ontario’s system of parks and protected areas. The parties to the agreement were the forest industry, the Partnership for Public Lands and the Ministry of Natural Resources. The Partnership for Public Lands is a coalition of three environmental interest groups – the World Wildlife Fund, the Federation of Ontario Naturalists and the Wildlands League.

The accord set out 31 commitments under which the massive expansion of parks and protected areas would occur. One of the 31 commitments (Accord Item 7) called for a process to be developed for any permanent increase in wood supply in the future to be shared between increased wood supply for the industry and further expansion of Ontario’s parks and protected areas.

After the signing of the accord, the Minister named an advisory board to assist in its implementation. Known as Ontario Forest Accord Advisory Board, (OFAAB), this board was comprised of representatives from the three parties to the original agreement. As part of its mandate, OFAAB developed a “Room to Grow” policy framework for sharing any future increases in wood supply.

In developing its policy framework, OFAAB was confident that permanent increases would be made to Ontario’s wood supply and that there would be room to expand both parks and protected areas and Ontario’s forest industry. The policy framework sets out how these future increases in wood supply will be shared between these two interests, and focuses on achieving three objectives:

- To define the gaps in the parks and protected areas system;

- To benchmark and secure the long-term supply of wood necessary for industrial processing; and,

- To share any permanent increases in wood supplies between filling gaps in the parks and protected areas system, and meeting the growing needs of Ontario’s forest industry.

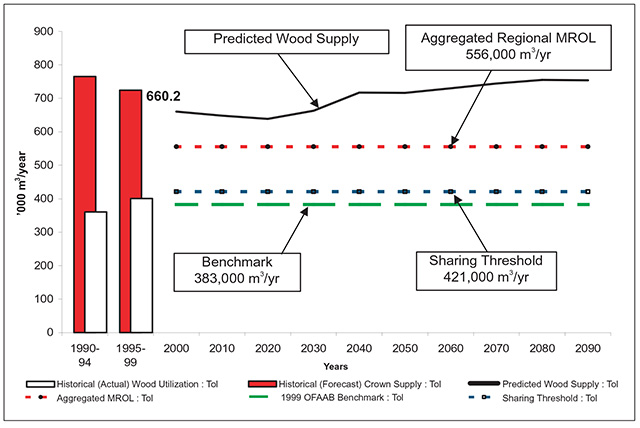

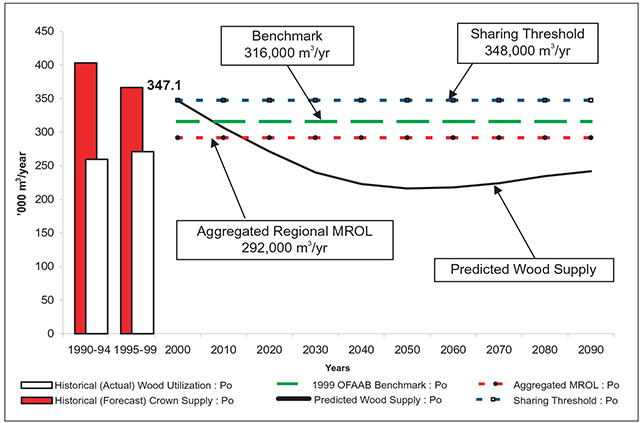

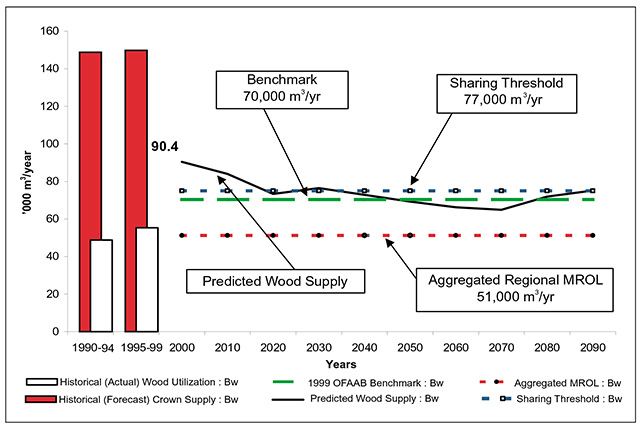

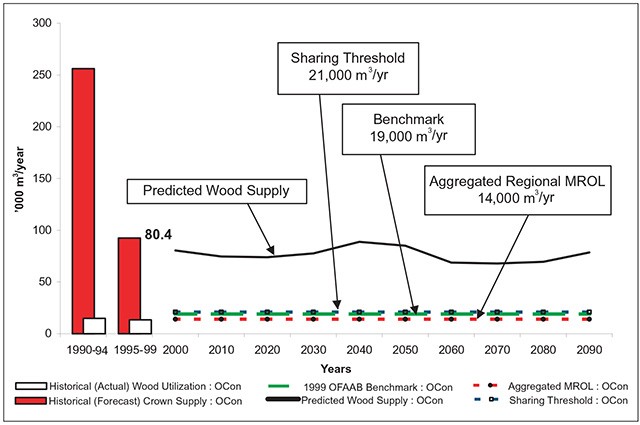

Table 1: OFAAB Benchmark Harvest Levels

| Species Group | NWR 1 | NER1 | SR1 |

|---|---|---|---|

| Spruce/Pine/Fir | 8,600 | 8,207 | 111 |

| White/Red Pine | 78 | 355 | 349 |

| Other Conifer | 24 | 27 | 19 |

| Poplar | 3,037* | 2,496 | 316 |

| White Birch | 95 ** | 229 | 70 *** |

| Tolerant Hardwoods | 0 | 241 | 383 |

| Total | 11,834 | 11,555 | 1,248 |

Note: Numbers presented represent the maximum utilization by region and species group between the period 1994 and 1999. (Source of data: TREES).

1MNR Administrative Region (000's m3/yr)

*NWR poplar benchmark includes 775,000 m3 of Crown commitments issued prior to March, 1999.

**NWR birch benchmark also includes 50,000 m3 of Crown commitments issued prior to March 1999.

***Correction to error which appears in the OFAAB Final Report benchmark table on page 13.

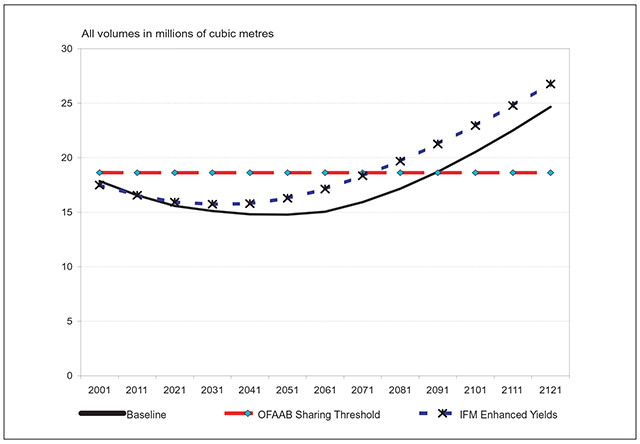

OFAAB chose the regional wood supply strategies as the instrument for benchmarking the fibre requirements of Ontario’s forest industry and for identifying the threshold that would initiate “Room to Grow” sharing discussions. Wood supply forecasting is not a precise science and OFAAB set the threshold 10 per cent higher than the industrial requirement benchmark as a safety margin to allow for errors. As the replacement for the regional wood supply strategies, the Provincial Wood Supply Strategy continues to benchmark the fibre supply requirements and the threshold level.

OFAAB defined the benchmark industrial wood requirement or wood supply as the highest annual harvest level that occurred during the five-year period ending March 31, 1999 for each of six major species groups, by region. This is the volume that OFAAB considered to be the basic wood supply requirement for Ontario’s forest industry. These benchmark wood supply volumes are shown in Table 1, by region and species group.

The Ontario Forest Accord and OFAAB’s proposed “Room to Grow” policy framework both contain important principles for securing the industry’s wood supply before further land withdrawals are made to expand Ontario’s parks and protected areas.

- Fundamental to the Forest Accord was the premise that there would be no long-term reduction in wood supply and no net increase in the cost of wood delivered to the mill as a result of the establishment of new parks and protected areas;

- The OFAAB “Room to Grow” sharing principles indicate that the sharing process is triggered when the long-term sustainable supply is above the sharing threshold (benchmark plus 10 per cent). (OFAAB, p.12);

footnote 6 - Decisions about sharing will be made at the forest management unit or woodshed level and must reflect the requirements of all licensees and companies having ministerial directives on that unit (OFAAB, p.14); and,

- Where sharing occurs, the process will be undertaken at the management unit and woodshed level and be designed to seek mutually beneficial solutions within the sprit and intent of the Accord (OFAAB, p.15).

The OFAAB baseline and the “Room to Grow” variables are presented in the wood supply graphs for each region in Part 2 of this report, and for each management unit and woodshed in Appendix 1. These data are current at the time of writing. The “Room to Grow” variables (the industrial benchmark, the sharing threshold and the long- term supply forecast) are to be updated annually. Long-term supply forecasts change as forest management plans are renewed. The industrial benchmark and associated sharing threshold may also change as “Room to Grow” sharing opportunities are realized. This updated information will be available upon request from the MNR’s Industry Relations Branch in Sault Ste. Marie.

MNR has accepted the OFAAB final report on “Room to Grow” and will complete a detailed implementation plan for the Forest Accord commitments, including identification of responsibilities and a proposed timetable. The Provincial Wood Supply Strategy may be adjusted pending the outcome of this implementation plan.

Methods and data sources

Each of the three regional reports within the strategy contain a comparison between the forecast of supply and the current demand level for each management unit, aggregated to the regional level. The data and analysis for each management unit, by species group, may be found in Appendix 1. Interested parties wishing to see the supply/demand situation for any one management unit are directed to Appendix 1.

The supply forecasts were taken directly from current approved forest management plans for each of the region’s management units. In each case the data source was the long-term forecast of available volumes, using the selected management alternative. The historical supply data that appears in bar form on the graphs in Part 3 were obtained from the management plans for each management unit for the two previous five-year terms. The historical harvest data, also in bar form on the graphs, was derived from provincial scaling data, both PTSBS and TREES.

On the demand side of the equation, the current Ministry Recognized Operating Levels for forest resource processing facilities (MROLs)

The OFAAB baseline for each of the three regions was determined by taking the highest annual volume cut in the five years ending March 31, 1999, for each of six species groups.

Assessment of the data reliability and the assumptions

Understanding the conclusions also requires an understanding of the data sources and their accuracy and reliability.

On the demand side, there is a strong degree of acceptance within the industry that MROLs accurately reflect current mill demand, but they do not necessarily represent future demand. The analysis in this document was done so as to determine the ability of the Crown forest to supply the existing industry. MROLs are considered to be accurate for this purpose. It is worth noting that MROLs established before 1999 are generally higher than actual consumption, a fact that should lead to an underestimate of surpluses, at least where surpluses have been forecast. Counterbalancing this to some degree is the fact that MROL data does not exist for very small mills (mills consuming less than 1,000 m3 annually)

It is important to point out that no attempt was made to forecast future demand levels, or to predict future trends in the forest products sector. Nor has the propensity of the industry to adapt to the type of wood that is available been factored in. In recent years new markets, new technologies and new methods have allowed the industry to produce highly desirable products from previously undesirable wood. This is perhaps the most important trend in wood utilization, both in Ontario and globally, and one that has prevented some of the supply shortages that have been predicted in the past from affecting the industry. This forecast of future demand and trends is outside of the scope of this strategy, however future demand and trends may be examined in other MNR initiatives such as the Forest Sector Strategy and may result in adjustments to the Provincial Wood Supply Strategy.

On the supply side, there is variability in the way individual management plans arrived at their long- term forecasts. All of them used current SFMM

Despite these challenges, it is safe to say that the major wood supply issues that have been identified are real issues and must be addressed. However, their magnitude and timing should not be considered precise. The quality of the information used to forecast long-term wood supply is identified in this document as one of the major issues, and several strategies are presented to address it. Refer to the Boreal Forest Issues and Strategies section found in Part 3 for more discussion on this topic.

Part 2. Regional reports

A. Northwest Region report

The forests of the northwest region

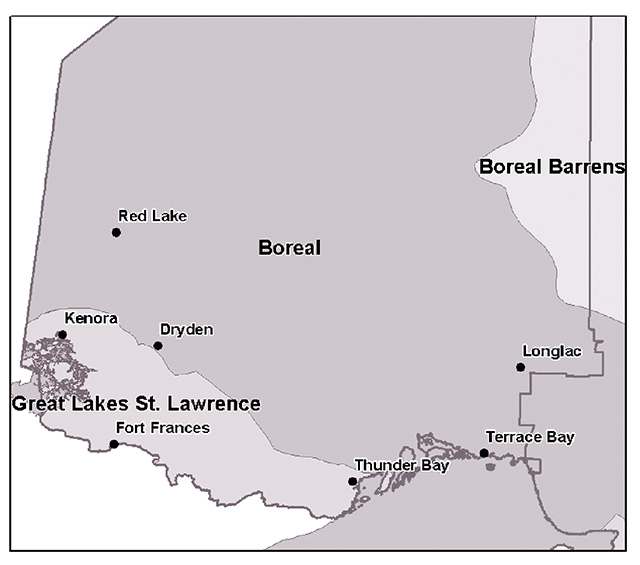

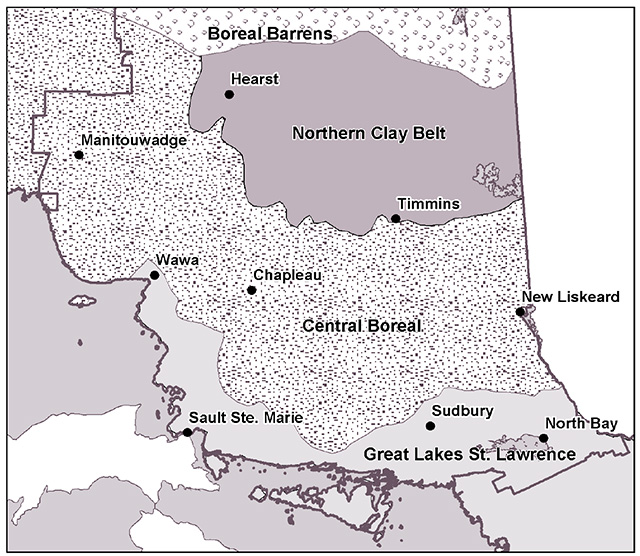

Northwest Region contains portions of two forest regions: the Boreal Forest and the Great Lakes-St. Lawrence Forest (GLSL). The Boreal Forest, accounting for the majority of area in Northwest Region, is characterized by extensive black spruce, jack pine, and balsam fir stands as well as mixed stands of conifer, poplar and white birch. Much smaller in extent, the Great Lakes-St. Lawrence Forest extends in a strip along the Ontario-Minnesota border west of Thunder Bay (see Figure 2) and features a diversity of conifer and hardwood species including white and red pine, red maple, yellow birch, and ash.

Three major species groupings are used in the Northwest Region to portray volume information: spruce-pine-fir (SPF), poplar and white birch (Po Bw), and white and red pine (Pw Pr). Most of the forest industry makes products that fall into these groupings. Examples are SPF lumber, SPF pulp and paper (Northern Bleached Softwood Kraft), poplar lumber, poplar oriented strand board, poplar pulp, and white or red pine lumber. White birch is used in pulp production and is just beginning to be used for lumber and consequently may warrant a separation from poplar as a grouping.

Wood processing facilities in the region are mostly large, commodity producing operations. Since the operations are so large, it has been left to the companies to make their own business arrangements to ensure appropriate species, log sizes, and log quality are delivered to the mills. For this reason, no attempt has been made to categorize species groups by product type.

Figure 2: Forest Regions of the Northwest

Enlarge figure 2: Forest Regions of the Northwest

The forest economy of the northwest region

Forestry is a key driver of the northern economy and is the major primary economic activity in Northwest Region. In this part of the province, the industry includes 13 sawmills (some of the largest in Ontario), 8 pulp and paper mills

A 1999 study completed by Lees and Associates

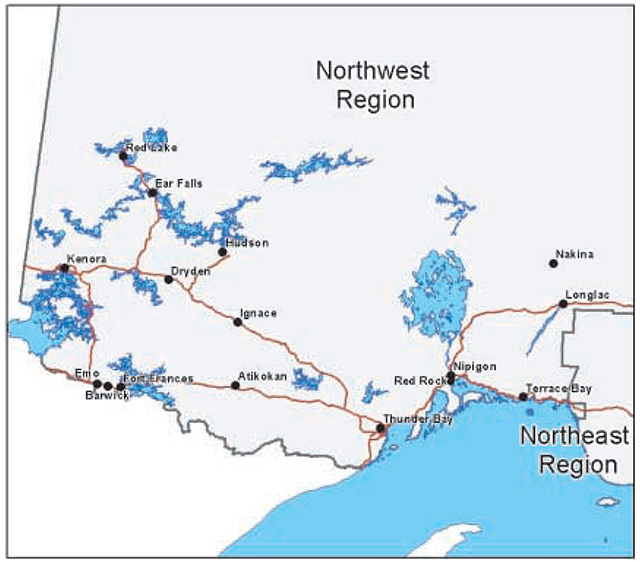

Figure 3: Communities with Mills in Northwest Region

Enlarge figure 3: Communities with Mills in Northwest Region

The study estimated that 15,300 full-time equivalent jobs were provided by the forestry sector. Some 14,900 people were engaged directly in forestry activities, while 400 additional government workers were employed in related fields associated with forest management and fire fighting. Payroll and benefits were estimated at $1.0 billion annually.

The industry is a major purchaser of goods and services. The 1999 study estimated $800 million is spent annually on goods and services within the region, and about $250 million on capital improvements, of which about $50 million was retained within the regional economy. Indirect employment, generated as a result of these expenditures, suggested 1.25 indirect jobs would result from each direct job. This multiplier effect resulting from 15,300 direct jobs would produce an additional 19,100 full-time equivalent jobs for a total of 34,400 jobs directly and indirectly associated with the forest industry. Evidence of the significant impact of the primary forest industry in the north is provided by the number of single industry communities that are wholly reliant on this sector for the jobs it provides.

The 1999 study further estimated that each 1,000 m3 of wood harvested generated 3.1 person years of employment, $164,000 in expenditures for labour, goods and services, and $55,000 in industry contributions to government. This is further evidence of the importance of forestry to the economy of the region.

Table 2: Companies and Mills in Northwest Region

| Company | Location | Products |

|---|---|---|

| Abitibi-Consolidated Company of Canada | Fort Frances | SPF pulp and paper; Po pulp |

| Abitibi-Consolidated Company of Canada | Kenora | Spruce paper |

| Abitibi-Consolidated Company of Canada | Thunder Bay | Spruce paper |

| Ainsworth Engineered Corp. | Barwick | Po oriented strandboard |

| Atikokan Forest Products Ltd. | Atikokan | SPF lumber and chips |

| Bowater Canadian Forest Products Inc. | Thunder Bay | SPF and Po pulp and paper |

| Bowater Canadian Forest Products Inc. | Thunder Bay | SPF lumber and chips |

| Bowater Canadian Forest Products Inc. | Ignace | SPF lumber and chips |

| Buchanan Northern Hardwoods Inc. | Thunder Bay | Po and Bw lumber and chips |

| Cascades Fine Papers Group Thunder Bay Inc. | Thunder Bay | Fine paper |

| Devlin Timber Company (1982) Limited | Kenora | SPF lumber, Pw Pr lumber and chips |

| Fibratech Manufacturing Inc. | Atikokan | Po and conifer particleboard |

| Great West Timber Limited | Thunder Bay | SPF lumber and chips |

| Kenora Forest Products Ltd. | Kenora | SPF lumber and chips |

| Kimberly-Clark Inc. | Terrace Bay | SPF and Po pulp |

| Levesque Plywood Limited | Nipigon | Po Plywood |

| LKGH Contracting Ltd. | Red Lake | SPF lumber and chips |

| Long Lake Forest Products Inc. | Longlac | SPF lumber and chips |

| Longlac Wood Industries Inc. | Longlac | Po plywood and strandboard |

| Manitou Forest Products Limited | Emo | SPF lumber, Pw Pr lumber and chips |

| McKenzie Forest Products Inc. | Hudson | SPF lumber and chips |

| Nakina Forest Products Inc. | Nakina | SPF lumber and chips |

| Norampac Inc. | Red Rock | Linerboard |

| Northern Sawmills Inc. | Thunder Bay | SPF lumber and chips |

| Weyerhaeuser Company Limited | Dryden | SPF and Po pulp and paper |

| Weyerhaeuser Company Limited | Ear Falls | SPF lumber and chips |

| Weyerhaeuser Company Limited | Kenora | Po strand lumber |

The long-term forecasts for industrial wood supply and utilization in northwest region

Past harvesting, current demand, and future supply

The following section describes past harvesting, current demand and future supply issues in Northwest Region on the basis of the following major species groups:

- Spruce-pine-fir;

- Poplar; and,

- White birch.

Spruce-pine-fir

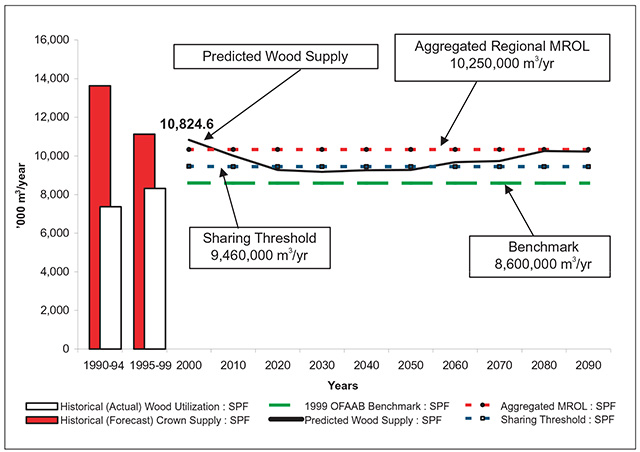

Figure 4 illustrates the relationship between wood supply and demand for spruce-pine-fir (SPF) at the regional level. It presents supply information obtained from forest management plans across the region, together with industrial demand and use.

This chart presents the dynamics of past use, current demand and future supply, all relevant factors in any discussion of wood supply and demand forecasting.

Historic Crown wood supply, shown as the black columns (red if viewed in colour version) on the graph, represents a summary of individual forest management plans averaged for the two five-year periods 1990-94 and 1995-99. This forecast suggests that Crown wood supply decreased during the decade of the 1990’s. The reduction is attributable in part to the impact of habitat management guidelines and the expansion of Wabakimi Park, which resulted in a smaller landbase for industrial forest use.

At the same time, however, actual wood utilization by the forest industry increased during the 1990's.

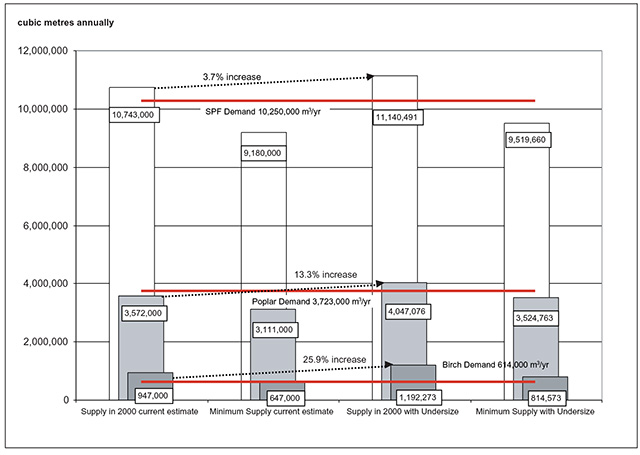

Figure 4: Comparison of Historical Forecast / Actual Harvest Levels with Current Demand and Future Harvest Wood Supply in Northwest Region – Spruce, Pine, Fir

The two white columns in Figure 4 illustrate the increasing use of Crown wood as a result of additional capacity associated with both existing and new facilities constructed during the decade. The final phases of SPF facility expansion ended in 2003 as certain sawmills finished expansion projects that began in 1998.

The demand for Crown origin SPF in 2000 was 10,250,000 m3/year, and this volume has been projected forward as a continuous demand. Included in the demand figure are the requirements of new and expanding mills that remain under construction. There is a delay in the actual harvest levels until these facilities achieve their full operating potential.

This analysis makes no attempt to separate the demand for SPF by product type (pulp and sawlogs). The sawmills and pulpmills in the region are highly integrated, meaning that sawmills receive a high proportion of the roundwood from which lumber and chips for pulpmills are produced. This level of integration means that sawmills are able to sort through large volumes of logs and treelengths in order to separate the larger diameter pieces for lumber production. In addition, high volume sawmills have an increasing ability to utilize smaller diameter logs in specialized saw lines. In combination, these sawmill characteristics have had the effect of reducing the need to separate wood demand and supply by product types.

The SPF projected wood supply shows a small surplus in 2000 (difference between 10,824,600 and 10,250,000 m3) that is projected to disappear. A gap between supply and demand becomes apparent by the year 2015.

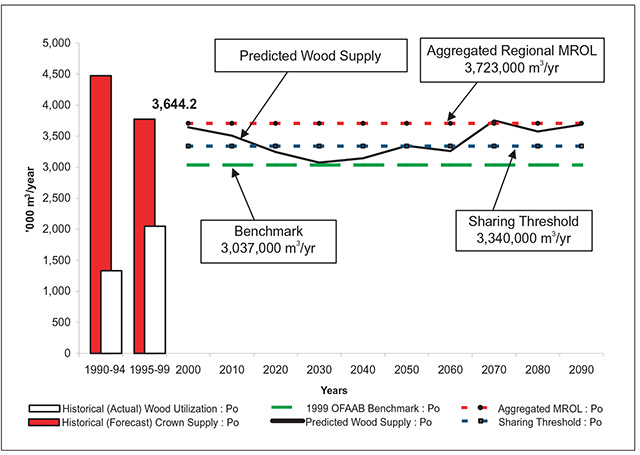

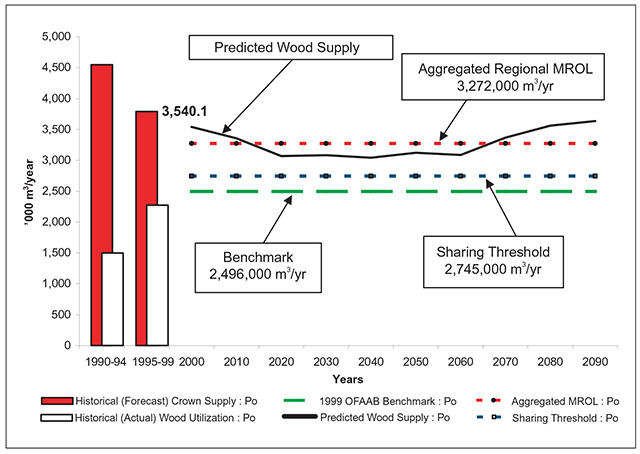

Poplar

The poplar comparison chart (Figure 5) is structured similarly to the SPF chart. However, there is a large difference between the average wood utilization in the 1995-99 period (approximately 2 million m3) and the current MROL level that is shown as 3.7 million m3. Since poplar had been under-utilized, a process was implemented to establish new facilities. The result was several new mills that boosted the poplar demand to the new level. The last of the new facilities is the strand lumber facility in Kenora, which was operational by October 2002. Actual poplar harvest levels will increase correspondingly as the mill achieves its operational potential during 2004.

Figure 5: Comparison of Historical Forecast/Actual Harvest Levels with Current Demand and Future Harvest Wood Supply in Northwest Region – Poplar

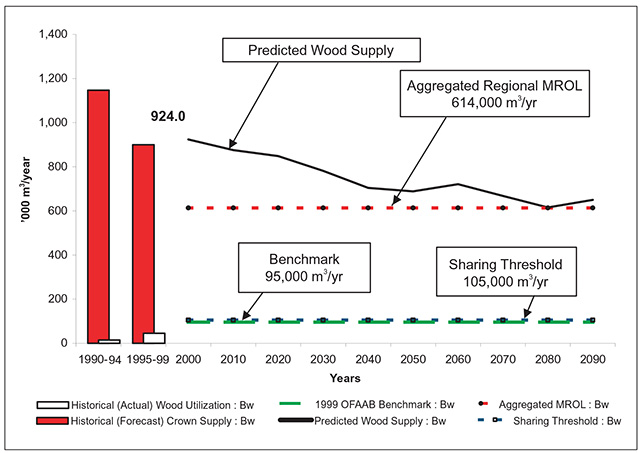

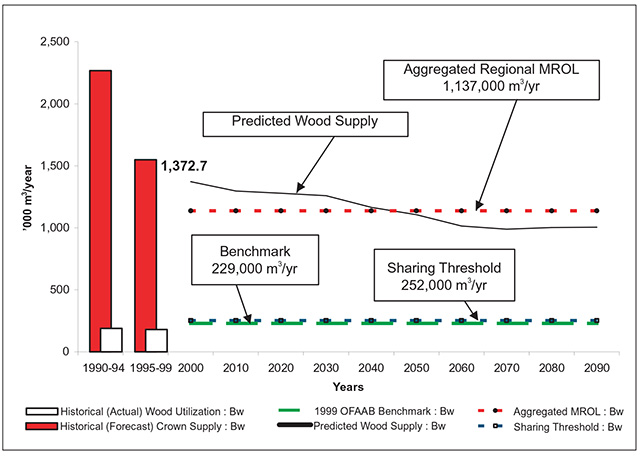

White birch

The comparison chart for white birch (Figure 6) shows a historically under-utilized species. The current demand for white birch is 614,000 m3/year and the industry is continuing to increase its use. The long-term supply of birch is greater than the demand, suggesting there is some room for growth in the use of this species.

The 1999 OFAAB benchmark was set very low in comparison to the current demand level. The process used to set the benchmark recognized the actual usage of birch during the 1995-99 period, which was much lower than the MROL levels. Actual usage of birch has continued to increase as those facilities to which the wood has been allocated have adjusted their processes accordingly.

Emerging utilization trends

In Northwest Region, there are a number of trends emerging with respect to wood utilization. Evidence suggests better use is being made of all boreal species. In addition, advances in harvesting technologies and mill diversification have had a profound influence on overall wood utilization throughout the region. These trends are discussed in detail under the following headings:

- Full Use of Allowable Harvest;

- Chips at Pulpmills;

- Integration Among Sawmills and Pulpmills; and,

- Increasing Utilization of the Available Harvest Volume.

Figure 6: Comparison of Historical Forecast/Actual Harvest Levels with Current Demand and Future Harvest Wood Supply in Northwest Region – White Birch

Full use of allowable harvest

Since 1994, MNR has been working toward the development of a full range of forest products and related economic opportunities throughout the Northwest Region. Unused volumes of timber were identified and businesses have been developed to use them. This has resulted in the building of new conifer sawmills at Ear Falls, Longlac and Nakina, a hardwood sawmill at Thunder Bay, a panel board mill at Barwick, a strand lumber mill at Kenora, and the expansion of conifer sawmills at Red Lake, Hudson, Atikokan, and Thunder Bay. While these new enterprises were being developed, the Wabakimi Park expansion was being finalized (1995) and Ontario’s Living Legacy was being implemented (1999). MNR’s development of economic opportunities and the expansion of Ontario’s system of parks and protected areas have resulted in a full allocation of the allowable harvest of the major species with the exception of white birch, which is approximately 50 per cent allocated.

Chips at sawmills

Pulpmills in Northwest Region have been increasing their capacity to accept chips instead of roundwood at the mill gate. With the exception of pulpmills that use grinders to produce pulp (spruce at Abitibi-Consolidated Company in Thunder Bay, Fort Frances and Kenora, and at Bowater in Thunder Bay; poplar at Abitibi-Consolidated Company in Fort Frances and Cascades Fine Papers in Thunder Bay), this has resulted in a very high proportion of pulpmills accepting only chips. The importance of this trend to the region as a whole is discussed more fully in the following section.

Integration among sawmills and pulpmills

Accepting chips at pulpmills has encouraged a high reliance on sawmills as a provider of raw materials.

When the recent Bowater sawmills are fully operational, about 72 per cent of the roundwood harvested in the region will pass through sawmills for conversion to lumber and chips. Before this development, sawmills had some difficulty selling all of the chips made during the production of lumber. This integration between sawmills and pulpmills has strengthened the sawmill industry by reducing uncertainty around the sale of chips, although it has increased the reliance of pulpmills on sawmills.

Increasing utilization of the available harvest volume

Bush chippers that convert full trees to chips by delimbing, debarking and chipping at the roadside allow almost all of the bole and larger branches of both conifer and poplar to be used. Despite the fact that extra care must be taken to separate sawlogs and veneer logs from treelengths before they are chipped, studies conducted by MNR for wood measurement and valuation purposes show that some 10 per cent more wood can be recovered from conifers, and up to 20 per cent more wood from poplar trees that are bush chipped.

The use of white birch has been increasing at pulpmills and in one sawmill in the region. The acceptance of birch sawmill chips by pulpmills has improved the economics of birch lumber production and white birch is expected to penetrate the lumber markets over time.

Throughout the region, mills have adjusted to changes in available wood supply. As a result of a limited supply of red and white pine, mills that relied on these species have diversified to others including jack pine and white spruce. In addition, larch that was once shunned by pulpmills has become a normal part of the conifer species used by some kraft pulpmills. Despite the fact that larch cannot be included by area sawmills in the SPF lumber definition, acceptance of larch has somewhat improved the wood supply in the region.

Overall, better utilization of tree species will lend itself to the development of merchandizing facilities (at mill yards or independent locations) where treelengths will be broken down into desirable products and then shipped to the appropriate mill. Likely merchandized products are veneer (mostly poplar and birch), sawlogs (mostly white, red and jack pine, white spruce, poplar and some white birch), oriented strandboard logs (poplar and white birch), and pulpwood of all species that may be shipped as roundwood or chipped. The smallest tops that were previously too short for transporting by pulp truck can be chipped and transported in vans. Merchandizing will not only get the right product and species to the right mill, it will also increase the total volume recovery from a harvested area.

B. Northeast region report

The forests of the northeast region

The forests of the Northeast Region include portions of three forest types: the Claybelt/ Northern Forest and the Central Boreal Forest, which both belong to the Boreal Forest Region, and the Great Lakes-St. Lawrence Forest Region (see Figure 7). These forest cover types conform to the broad soil and climatic zones found in this part of the province.

Claybelt/northern forest

This type of forest is defined by its deep lacustrine clay soils with organic accumulations on the lowland sites. It is dominated by large expanses of lowland black spruce in the north with an increasing proportion of uplands dominated by aspen poplar in the south. White birch, larch, balsam poplar and balsam fir are found to a lesser extent throughout the area. Infrequent areas of sandy and coarse soils are dominated by jack pine.

Over the last 100 years, human activity (settlement, fires and logging in particular) has had a profound effect on the forests of this area. One result is the increased prevalence of poplar in the region. During the 1980s and 1990s, forest managers set planning objectives to reverse this trend through active conifer silviculture programs. There has, however, been an increasing emphasis on natural regeneration and mixed wood management in the last five years.

The forest tent caterpillars have heavily defoliated the aspen forests in this area over the past several years. This defoliation has been linked to approximately 450,000 ha of severely declining aspen. As of this writing, the full impact on long term poplar wood supply in the region has yet to be determined.

Central boreal forest

The Central Boreal Forest region is characterized by till deposits, sands, and coarse soils, together with frequent rock outcrops and ridges. Here a moderate climate prevails and growing conditions tend to be more favourable and more productive than the claybelt described above.

Mixed forests of conifer and hardwoods dominate the landscape, together with extensive forests of even-aged jack pine on well-drained sandy soils. This forest area contains a greater diversity of tree species than the claybelt and includes a significantly larger proportion of white birch. Toward the southern reaches of this area, the forest exhibits a transition toward species found in the Great Lakes-St. Lawrence Forest. Here, white and red pine and hard maples are found in scattered locations.

Figure 7: Forest Regions of Northeast Region

Similar to the claybelt, the central boreal forest has succeeded toward a higher proportion of hardwoods, including both white birch and poplar. Limited silvicultural activity following forest harvesting during the period from about 1900 to about 1975 produced sizeable areas of degraded, low-volume hardwood forest.

Silvicultural activity and the success of forest regeneration programs has increased significantly since the 1970s. This positive trend began with larger silvicultural budgets as a result of the Forest Production Policy of the 1970s, and continued with the signing of Forest Management Agreements in the 1980s and the advent of the Forest Renewal Trust Fund in the 1990s.

Great Lakes-St. Lawrence forest

The Great Lakes-St. Lawrence Forest is characterized by a transition from boreal forest types in the north, to increasing amounts of white pine/red pine and tolerant hardwoods in the south. The underlying geology consists of deep till soils and rocky broken terrain with shallow coarse soils. While the area contains a diverse mix of species, many of the tolerant hardwoods are of low grade. This has resulted from past high-grading practices and the fact that the hardwoods are located near the northern limit of their climatic range.

Over the past 100 years or more, the amount of white and red pine has been greatly reduced as a result of three key factors:

- Reduced fire prevalence in the forest, which leads to succession toward tolerant hardwoods;

- Past harvesting practices which concentrated on removing high-value trees; and,

- A subsequent lack of regeneration of the pine.

The issue of white and red pine regeneration has been addressed in recent forest management plans with objectives included for pine restoration. However, the existing pine resource is old and not as prevalent as in the past. Hard maple and yellow birch stands have been degraded through successive high-grading operations. This has begun to be addressed within the last 10 to 20 years through the establishment of proper tree-marking standards and stand improvement efforts. This change in management means there will be a continued shortage of sawlog supply relative to the amount of low-grade hardwoods, at least for the short term, but the supply should improve in the long term.

Species groups and product categories

There are five major species groupings that are used in the Northeast Region to portray volume information: spruce-pine-fir (SPF), poplar (Po), white birch (Bw), white and red pine (Pw/Pr), and tolerant hardwood (Mh/By). Most of the forest industry makes products from these species groupings. Examples are SPF lumber, SPF pulp and paper (Northern Bleached Softwood Kraft), poplar veneer panels, poplar oriented strandboard, poplar pulp, white or red pine lumber, and maple and birch veneer and lumber. A small proportion of white birch has traditionally been harvested for veneer, but this species is just beginning to be used for OSB and other specialty products.

Wood processing facilities in the region are mostly large, commodity-producing operations. Since the operations are so large, it has been left to the companies to make their own business arrangements to ensure the appropriate species, log sizes and log quality are delivered to the mills. For this reason, no attempt has been made to categorize species groups by product in this part of the report. However, MNR staff do work with individual companies to ensure wood directives set out by the Minister are met, when this becomes a concern. Although there is some consensus on product quantities or percentages in some sectors, this information has not generally been incorporated into forest management planning, and so this product information is not consistently available for our analysis of wood supply in the Northeast Region. Therefore, product supply issues have not been closely examined in building the Northeast strategies. This issue may be investigated in future versions of the strategies and has been included in Part 5 on Future Considerations.

The forest economy of the northeast region

Forestry is a key driver of the northern economy and the forest industry is the major primary economic activity in the Northeast Region. In this part of the province, the industry includes 24 sawmills (ranging from large SPF mills to small hardwood mills in the southern part of the region), five pulp and paper mills, three oriented strandboard mills, six veneer/veneer panel mills, and three composite board mills. See Figure 8 and Table 3 for the location and brief description of significant Crown wood-using facilities. A more extensive listing of forest resource processing facilities in Ontario is currently available on MNR’s Ontario’s Forests website within the forest industry page. In addition, woodlands, harvesting, transportation and silviculture operations occur throughout the region.

The forest industry is a significant employer in the majority of the communities throughout Northeast Region. Not only does the industry offer its employees relatively secure employment tenure, but it pays well and produces significant economic spin-off benefits to virtually every community in the region.

The industry is also a major purchaser of goods and services and often an important supporter of communities through both the tax base and voluntary contributions. In 1999, a study was completed by Lees and Associates that examined the economic contribution of the primary forest products industry to Northwestern Ontario. The study estimated that each 1,000 m3 of wood harvested generated 3.1 person years of employment, $164,000 in expenditures for labour, goods and services, and $55,000 in industry contributions to government.

Figure 8: Communities with Mills in Northeast Region

Table 3: Companies and Mills in Northeast Region

| Company | Location | Products |

|---|---|---|

| Abitibi-Consolidated Company of Canada | Iroquois Falls | Spruce newsprint and paper |

| Birchland Veneer Limited | Thessalon | Maple & birch veneer |

| Boniferro Mill Works Inc. | Sault Ste. Marie | Maple, birch & oak lumber |

| H & R Chartrand Limited | Noelville (Sudbury) | SPF & white/red pine lumber |

| Cheminis Lumber Inc. | Larder Lake (Kirkland Lake) | SPF lumber and chips |

| Levesque Plywood Limited | Hearst | Hardwood overlay plywood; poplar and birch veneer |

| Levesque Plywood Limited | Hearst | Particle board |

| Columbia Forest Products Ltd. | Rutherglen (Mattawa) | Maple & birch veneer |

| Domtar Inc. | Espanola | Softwood and hardwood bleached pulp |

| Domtar Inc. | Nairn Centre (Espanola) | SPF lumber and chips |

| Domtar Inc. – McChesney Division | Timmins | SPF lumber and chips |

| Domtar Inc. | Chapleau | SPF lumber and chips |

| Domtar Inc. | White River | SPF lumber and chips |

| Dubreuil Forest Products Limited | Dubreuilville | SPF lumber and chips |

| Elk Lake Planing Mill Ltd. (Liskeard Lumber & Domtar) | Elk Lake | SPF lumber and chips |

| Excel Forest Products | Opasatika | SPF lumber and chips |

| Extreme Timber | Mattice (Hearst) | Cedar mill (shingles) |

| Forest Ply Industries | Blind River | Poplar and softwood veneer plywood |

| R. Fryer Forest Products Limited | Monetville (Sudbury) | White/red pine, maple, birch & SPF lumber |

| Gervais Forest Products Ltd. | Falconbridge (Sudbury) | Maple, birch, white/red pine & SPF lumber |

| Gogama Forest Products Inc. | Ostrom | SPF lumber and chips |

| Goulard Lumber (1971) Ltd. | Sturgeon Falls | White/red pine and SPF lumber |

| G-P Flakeboard Company | Sault Ste. Marie | MDF panels |

| Grant Forest Products Inc. | Timmins | Poplar and birch oriented strandboard |

| Grant Forest Products Inc. | Englehart | Poplar and birch oriented strandboard |

| Isidore Roy Limited | Sturgeon Falls | SPF and white/red pine lumber |

| Lahaie Lumber Ltd. | Alban (Sudbury) | White/red pine, SPF, maple & birch lumber |

| Lecours Lumber Co. Limited | Calstock (Hearst) | SPF lumber and chips |

| Little John Enterprises Ltd. | Timmins | SPF lumber and chips |

| Mainville Lumber Company Limited | Chelmsford (Sudbury) | SPF & white/red pine lumber |

| Marathon Pulp Inc. | Marathon | SPF & poplar kraft pulp |

| Midway Lumber Mills Ltd. | Thessalon | Maple, birch, white/red pine & SPF lumber |

| Olav Haavaldsrud Timber Company Ltd. | Hornepayne | SPF lumber and chips |

| Nipissing Sawmill Ltd. | North Bay | Maple, birch, white/red pine & SPF lumber |

| Norbord Industries Inc. | Cochrane | Hardwood overlay plywood |

| Northern Pressure Treated Wood Ltd. | Dobie (Kirkland Lake) | Poles & lumber – red & jack pine |

| Pineal Lake Lumber Company Ltd. (Mason Windows) | Chapleau | Specialty white pine lumber |

| Portelance Lumber (Capreol) Ltd. | Capreol | White/red pine & SPF lumber |

| Precut Hardwood Inc. | North Bay | White birch pallet stock & fire wood |

| St.Marys Paper Ltd. | Sault Ste. Marie | Spruce, fir and poplar supercalendered paper |

| Superior Hardwood Veneer Ltd. | Sault Ste. Marie | Maple & birch veneer |

| Tembec Industries Inc. | Smooth Rock Falls | SPF kraft pulp |

| Tembec Industries Inc. | Cochrane | SPF lumber and chips |

| Tembec Industries Inc. | Kapuskasing | SPF pulp and paper |

| Tembec Industries Inc. | Kapuskasing | SPF lumber and chips |

| Tembec Industries Inc | Hearst | SPF lumber and chips |

| Tembec Industries Inc. | Kenogami | SPF lumber and chips |

| Tembec Industries Inc. | Mattawa | Maple, other tolerant hardwoods, white birch, white/red pine & SPF lumber |

| Tembec Industries Inc. | Timmins | SPF lumber and chips |

| Tembec Industries Inc. | Chapleau | SPF lumber and chips |

| Uniboard New Liskeard Inc. (Rexwood) | New Liskeard | Composite board |

| Weyerhaeuser Company Ltd. | Limer (Wawa) | Poplar & birch oriented strandboard |

The long-term forecasts for industrial wood supply and utilization in northeast region

Past harvesting, current demand, and future supply

The following section describes past harvesting, current demand and future supply issues in Northeast Region on the basis of the following major species groups:

- Spruce-pine-fir;

- Poplar;

- White birch;

- White pine/red pine; and,

- Tolerant hardwoods.

Spruce-pine-fir

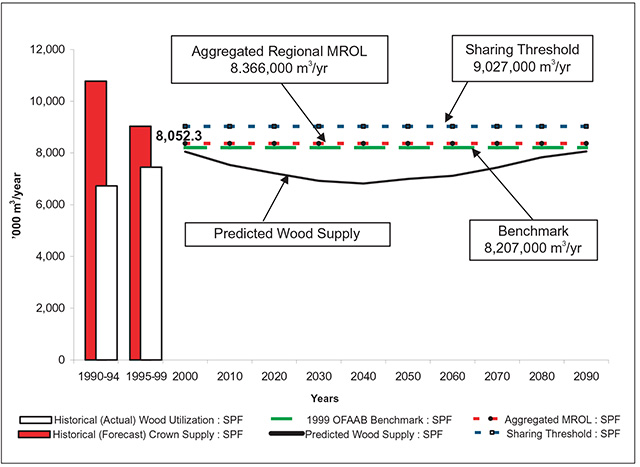

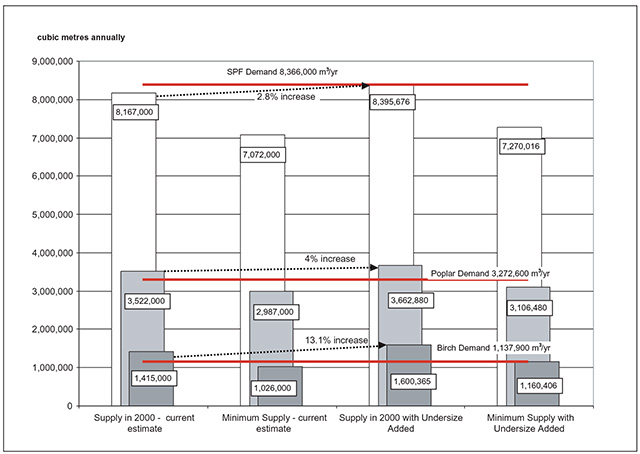

The wood supply and demand chart, (see Figure 9), illustrates the relationship between wood supply and demand for spruce-pine-fir (SPF) at the regional level. It presents supply information obtained from forest management plans across the region, together with industrial demand and use information.

Crown wood supply, shown as the black columns (red if viewed in colour version) on the graph in Figure 9, represents a summary of individual forest management plans averaged for the two five-year periods 1990-94 and 1995-99. The five-year wood supply projections have been steadily declining for the past decade. This decline in available harvest volume is attributed to five factors:

- Land withdrawals from the area available for forest management;

- New forest management guidelines;

- More rigorous application of existing guidelines;

- Past harvesting and silviculture practices; and,

- An aging forest and a consequent general decline of merchantable volumes due to an overmature forest.

At the same time however, actual harvest level has been increasing during the 1990's (white columns on graph). This reflects a general trend toward more complete utilization of the available supply, stronger market demand, and better prices for lumber and paper.

The demand for SPF in the Northeast Region was 8,366,000 m3/year in 2000, (based on MROLs), and this volume has been projected forward as a continuous demand. The SPF wood supply currently equals the demand. Within five years, however, wood supply, based on current modelling, is predicted to decline below demand.

The gap that has been forecast between wood supply and the industrial demand for fibre has been recognized and debated for the last decade or more.

Figure 9: Comparison of Historical Forecast/Actual Harvest Levels with Current Demand and Future Harvest Wood Supply in Northeast Region – Spruce, Pine, Fir

While it results from a number of factors, the fundamental reason for this approaching gap is a significant age class imbalance. The dominant age class on the landscape of Northeastern Ontario has been mature and is now slipping from mature to over-mature. The level of industrial wood consumption has increased over the past 50 years in response to this abundance of mature forest. The philosophy has been “use it rather than lose it to natural decline.” Forest managers have attempted to achieve a balance, at the management unit level, between consuming the surplus of old wood, retaining a consistent supply of wood in the long term and retaining mature forest for non- consumptive forestry objectives. Even so, forest management plan modelling forecasts that the existing industrial capacity will exceed the supply of wood beginning about 10 years hence.

The predominance of old forest in the region stands in marked contrast to the relative scarcity of mid- aged forest (i.e. 20 to 60 years old). Ironically, this aging of the forest can be related to a conservative approach to wood supply in the first half of the century together with an aggressive and successful fire suppression strategy. Prior to 1970, human disturbance in the forest through timber harvesting was considerably less than today, while fire control has reduced the natural renewal of forests over the past 50 years. Less human disturbance in the forest meant that forests were not renewed at today’s levels. Rates of forest renewal prior to 1980 were insufficient to produce the supply of young conifer forest that will be needed to sustain current utilization levels during the next 20 to 40 years. As a result, forest managers will need to be innovative to maintain current wood supply levels. The strategies included in this document will assist with this innovation. Individual companies will address the forecast wood supply shortages through their own sets of strategies.

There are a number of factors that influence the relationship between wood supply and demand. Some of these include:

- Economic, social and technological changes;

- Policy decisions;

- Changes in inventory, growth and yield estimates; as well as,

- Impacts resulting from international market forces.

Economic and technological changes can affect wood supply by increasing the utilization of available fibre (e.g. smaller tops, harvesting of low volume stands and utilization of species like white birch). However, societal demands can also influence the supply and demand equation if concerns are raised respecting industrial use of the public forest resource. The movement toward ecosystem-based management of the forest has reduced the supply of wood available to industry. For example, it has led to more protected areas, an emphasis on wildlife habitat management and the retention of older forest age classes.

There has been growing societal pressure to increase the protection of non-timber values and accommodate the needs of other users of the forest. The resulting policy changes affect wood supply and demand. The development of new forest management guidelines, together with the more rigorous application of existing guidelines has reduced available wood supply in the past, and may be expected to depress future wood supply as new forest management plans are written. Future policy changes or increases in wood utilization are not commonly factored into wood supply modelling for forest management planning. The strategies presented in Part 3 look at opportunities both to fill the gap between supply and demand and to replace volume that may be lost to industry as a result of future policy changes.

The relationship between wood supply and demand is also affected by changes in inventory, growth and yield estimates, and methods of analysis. Methods of analysis have become increasingly complex as managers apply advanced modelling techniques to document the interaction of natural and human forces in the forest. The development of spatial decision support systems may be expected to bring new changes to the supply equation.

In addition to economic, technological and social change and changes to the policy and analytical environment, wood supply and demand is affected by international market forces. In Ontario, as elsewhere, the wood products industry competes in an international market to sell its products. The industry must constantly strive to improve its efficiency and increase its productive capacity in order to survive. These efforts require continued operational improvements in efficiency and effectiveness at the individual mill level and may lead to requests for an increase in total fibre supply, an increase in mill productivity, or a rationalization of wood flow among mills. Forest industry certification is increasingly affecting how industry operates in the forest and may have an influence on wood supply.

Supply numbers are determined by a consultative process that involves setting objectives, conducting forest management modelling, and analyzing management alternatives on individual management units. Each management unit has its own characteristics, marked by times of surplus and supply shortages. Individual mills will be challenged to address the supply surpluses and shortfalls. While this report recognizes these challenges, it focuses on region-wide strategies and does not address individual mill supply issues. However, the strategies will often be implemented at the local level and will help mitigate local supply issues.

For the Northeast Region, the approaching gap between wood supply and demand is most significant for the conifer-based industry. Similar concerns however, are also an issue for the poplar-based industry. These challenges are discussed in detail below.

Poplar

As illustrated in Figure 10, the relationship between wood supply and demand for poplar is similar to that of SPF, with an anticipated supply gap occurring within 15 years. The reasons for this supply gap are the same as those described above for the SPF supply gap. However, there are nine significant differences between these two major species groups:

- Shorter History of Harvesting: Poplar harvesting began about 40 years ago and only became significant in the past 20 years. The knowledge of silvics and growth and yield for this species is also more recent. Generally, poplar was given little management attention until the beginning of the 1990s.

- Harvesting and Silviculture Practices: Harvest and silviculture practices for all species groups from the 1920s to about 1980 created a greater presence of poplar and birch on the landscape, both in pure and mixed forest stands. This has created a variety of mid-age forests. Some stands are well-stocked and very productive, while others are poor quality, low-volume stands growing off-site or degraded through past high-grading practices.

- Rapid Decline in Poplar: Poplar forests tend to break-up and lose both quality and volume rapidly once they pass maturity. As a result, poplar generally does not store well on the stump, although there are large geographic differences with respect to age of decadence. This characteristic of rapid decline accentuates the problem of determining reliable volume estimations as upland boreal forests age.

- Forest Management Dynamics: Mixed forests of poplar and conifer are important to the supply for both species groups and are often the most productive sites in the boreal forest. Because the consuming mills generally use only one species group, there is an ongoing tension over the management of these forest types. The management and dynamics of these forest types are more complex and less understood than those of the pure species forest types.

- Large Areas of Decadent Poplar: Large areas of poplar which developed after massive fires in the early part of the 20th century are beginning to become decadent. They will pass quickly through forest succession processes over the next 20 years.

- Implications of Poplar Decline: The forest tent caterpillar has unexpectedly become a significant factor in the health of poplar. Poplar stands across extensive areas of the Claybelt Forest of the northeast have experienced 60 to 90 per cent mortality. There are indications that this infestation is continuing to move throughout the northeast and may cause unprecedented reductions in poplar wood supply. Analysis carried out in 2001 indicates a supply reduction of about 150,000 m3 during the low point in the supply forecast - about 20 years hence. Surveys conducted in 2002 and 2003 indicate a further one-third increase in area of poplar decline each year and therefore a further reduction in long- term wood supply. The degree of the long-term impact on poplar supply is uncertain and needs to be further investigated. The success of poplar regeneration in the areas of decline is also needs to be assessed. Natural regeneration of poplar cannot be assumed in these areas of poplar decline since the root systems of the mature trees are usually depleted of their energy reserves.

- Commitments to Industry: Poplar commitments to industry were greatly increased during the 1990s. That capacity has not been completely realized. Although supply does not drop below the OFAAB Benchmark or Sharing Threshold, it does drop below the level required to meet current industry commitments.

- Poplar Supply & Commitments: When examined on a regional basis, both the projected supply of poplar and the poplar commitments to industry exceed the OFAAB Benchmark and Threshold level for sharing under the “Room To Grow” policy framework. (See the discussion of birch below.)

- Private Land Wood Supply: From the 1990s to the present, the industry using poplar in the Northeast has consistently substituted wood harvested from private land for Crown sources. This unregulated harvest on private land may not be sustainable, and the industry will likely require the full use of its Crown poplar commitments within a few years. In the meantime, Crown commitments are not being fully utilized.

Figure 10: Comparison of Historical Forecast/Actual Harvest Levels with Current Demand and Future Harvest Wood Supply in Northeast Region – Poplar

Poplar shares many of the same supply problems as SPF, in particular, the age class imbalance. While poplar grows and regenerates quickly after harvest, it also declines quickly, resulting in supply predictions that are less certain.

In the Northeast Region, poplar is used for veneer (i.e. plywood), composite (i.e. OSB), and pulp. Although this report has not differentiated between these products, individual forest management plans set objectives for each of these product types. Shortages of veneer supply are likely to occur before any shortages in composite or pulp material. This is the result of the aging and decline of the current poplar resource, combined with the probability of a reduced age of harvest in the future. As with the conifer based industry, economic and technological changes are expected to increase the use and utilization of available fibre.

White birch

The comparison chart for white birch (Figure 11) shows a historically under-utilized species. Attention to its growth and yield, and its management, lag behind both SPF and poplar. Supply estimates are consequently less reliable than the other major commercial species.

A large amount of the white birch in the Northeast Region exists in high-graded stands and poor quality second-growth forest, or low-quality stands growing on shallow soils. Some of the forecast wood supply decline noted in Figure 11 is due to objectives within forest management plans to convert these poor quality forest areas to conifer and mixed woods.

Figure 11: Comparison of Historical Forecast/Actual Harvest Levels with Current Demand and Future Harvest Wood Supply in Northeast Region - White Birch

The majority of the birch demand, shown as the regional MROL, involves recent commitments to industry. This industrial use is forecasted and mill capacity is not yet in place, causing a short-term surplus of this product. Traditionally, birch areas have been harvested both for the conifer content within the stands and the small percentage of veneer quality logs – often less than one per cent – but not the lower grade of logs. The majority of the birch has not been used in the past. However, the trend toward complete utilization of the birch resource will produce opportunities for better quality birch regeneration. This change will also increase the amount of SPF and poplar produced as incidental volume.

The Ontario Forest Accord Advisory Board benchmark for white birch is set at 229,000 m3/year in the Northeast Region. Since the long-term harvest supply for this species exceeds the “Room to Grow” threshold by a factor of more than four times, there may be implications for sharing wood supply as described in the “Room to Grow” policy framework. This may have implications for the projected industrial supply of this species. A similar situation exists for poplar and white and red pine in the Northeast Region. Discussions on sharing for these species may proceed once the Forest Accord implementation package and details have been finalized and approved.

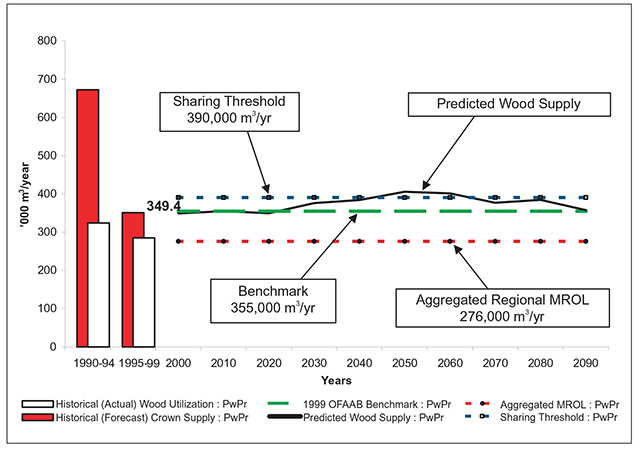

White pine/red pine

The occurrence of white and red pine across the region is limited. However, it is a significant high- value product for a number of sawmills in the Highway 17 corridor between North Bay and Sault Ste. Marie. The current demand for sawlog quality pine exceeds supply, even though Figure 12 indicates supply and demand are approximately equal. The advanced age and marginal state of the pine resource has created a high ratio of cull and pulp grade wood compared to sawlogs. With a limited pulp market, there is a surplus of low-grade pine.

Figure 12: Comparison of Historical Forecast/Actual Harvest Levels with Current Demand and Future Harvest Wood Supply in Northeast Region - White Pine/ Red Pine

Figure 12 indicates that the predicted wood supply approximately equals the sharing threshold. Unfortunately there is a small surplus of low-grade pulp wood and a real shortage of sawlog pine. Also, a significant proportion of the pine in the Northeast Region has been harvested traditionally from non- pine stands (i.e. incidental within other forest types), and this pine is becoming increasingly unavailable because of tree retention guidelines. This will further accentuate the future shortage of sawlog pine.

Although pine remains an important part of the sawmill business, most mills in the Northeast Region that traditionally relied on white and red pine have diversified to a wide range of species including jack pine and white spruce.

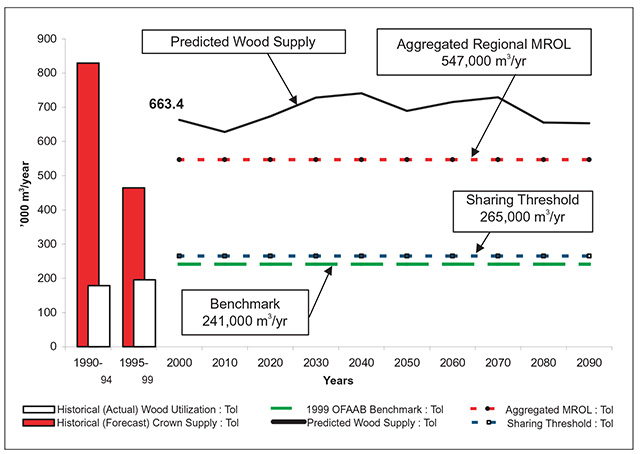

Tolerant hardwoods

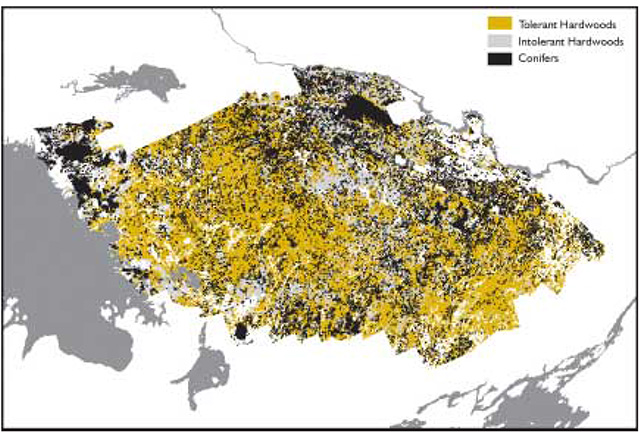

Like white and red pine, tolerant hardwoods make up only a small part of the Region’s forests, accounting for less than five per cent of wood supply overall. The productive tolerant hardwood sites occur only in the Great Lakes-St. Lawrence Forest along the southern fringe of the Northeast Region, as shown on Figure 13. For many years, tolerant hardwoods have been the source of supply for sawmills and veneer mills along the Highway 17 corridor, stretching from Mattawa to Sault Ste. Marie.

Figure 13 shows the current hardwood supply to be well above the level of demand, and well above the “Room to Grow” Sharing Threshold. As in the Southern Region, however, this surplus is confined to low-grade hardwoods, while veneer and sawlog supply is in a deficit situation. The problem stems from the fact that these species are growing at the northern extremity of their range, where log quality is generally poor. This deficit has been aggravated by high-grade logging practices used in the past. Today, proper tree marking and stand management practices have further constrained the short-term veneer and sawlog supply for the remaining facilities, since application of these practices have increased the ratio of pulp wood to sawlogs.

The solution to the veneer and sawlog shortage lies in developing new markets for the surplus low- grade material. The recent NE/SC Hardwood Project was unsuccessful in its attempt to attract new industries to use this surplus wood, or to have one of the existing pulp users expand production.

A more complete discussion of tolerant hardwoods may be found in the Southern Region section of this document. Part 3 contains strategies developed for the hardwoods and pines of the Great Lakes-St. Lawrence area of the Northeast Region. The issues and strategies for tolerant hardwoods and white and red pine may be examined more thoroughly in future versions of the Provincial Wood Supply Strategy.

Emerging utilization trends

In the Northeast Region, there are a number of trends that are emerging with respect to wood utilization. Evidence suggests better use is being made of all species. In addition, advances in harvesting technologies and mill diversification have had a profound influence on overall wood utilization throughout the region. These trends are discussed more fully under the following headings:

- Full Use of Allowable Harvest;

- Chips at Pulpmills & Integration With Sawmills;

- Increasing Utilization; and,

- Minor Species.

Full use of allowable harvest